InsightsMonthly Market Wrap – January 2026

February 05, 2026 • 7 MIN READ

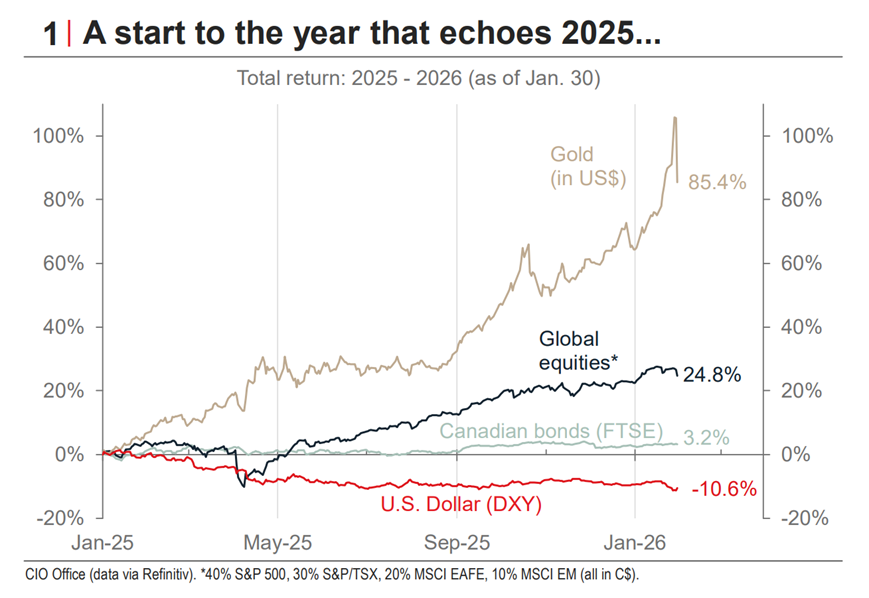

January opened 2026 with a clear message: the shifting dynamics that characterized much of 2025 are not only persisting, they are intensifying. Against a backdrop of escalating geopolitical instability, including military operations in Venezuela, heightened U.S.–Iran tensions, and aggressive trade rhetoric aimed at allies and partners , financial markets extended several of the prior year’s key trends. International equities outperformed, the U.S. dollar weakened further, and gold surged to new record highs. Importantly, while political uncertainty dominated headlines, economic fundamentals remained broadly supportive, with growth data exceeding expectations, inflation stabilizing near target, and corporate earnings holding firm. The widening gap between solid macro conditions and an increasingly unpredictable policy environment suggests investors will need to navigate 2026 with both discipline and flexibility.

Equity Markets

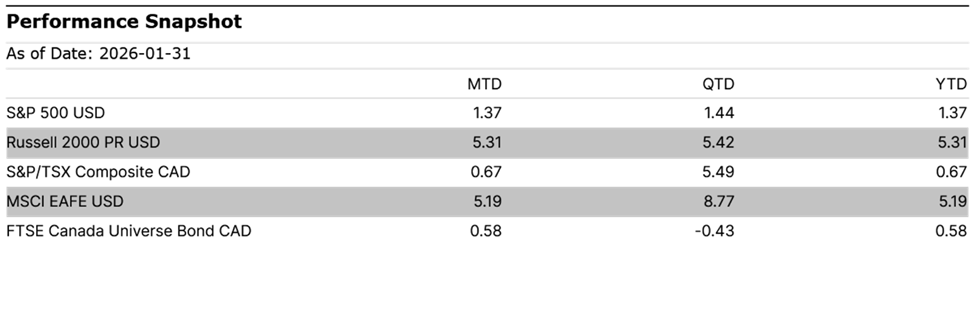

Equity markets posted gains in January, but the most notable feature was the significant geographical dispersion in returns. The rotation away from U.S. dominance that began in 2025 accelerated meaningfully, with overseas markets outperforming on nearly every dimension. See the performance table below:

In the United States, the S&P 500 returned 1.37% in U.S. dollar terms, but this modest headline number masked notable turbulence. Tariff threats on European countries over Greenland triggered the worst single-day session since April 2025, though markets recovered on news of a framework deal with NATO. The equal-weighted S&P 500 gained 3.4%, suggesting broader participation beyond mega-cap technology. Small-cap stocks also showed renewed strength, with the Russell 2000 rising 5.4%, a potential signal that investors expect pro-domestic-growth policies ahead of midterm elections.

Canadian equities benefited from the country’s resource-heavy composition. The S&P/TSX gained 0.67%, led by Materials (+8.9%) and Energy (+10.6%), which surged on rising commodity prices and gold strength. However, Information Technology (-17.6%) and Consumer Discretionary (-5.3%) struggled, reminding investors that sector concentration cuts both ways.

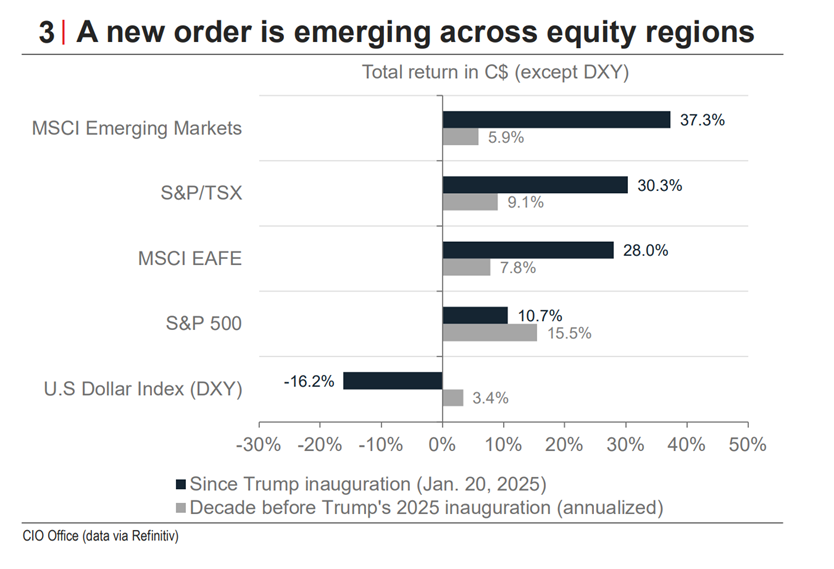

International equities were the standout performers. The MSCI EAFE returned 5.2% while emerging markets delivered an exceptional 8.9%. European and Japanese markets benefited from improving earnings and attractive valuations, while emerging markets were supported by a weakening U.S. dollar and AI-driven demand in Asian technology hubs. One year after the inauguration of the 47th U.S. President, the geopolitical turbulence has not disrupted the global equity bull market — but it has fundamentally reshuffled performance rankings across regions, to the detriment of U.S. assets.

Fixed Income and Credit

Fixed income was relatively quiet in January, with the Canadian bond universe returning 0.6%, recouping roughly half of December’s losses. Corporate bonds gained 0.9% as credit spreads remained well-contained.

Both the Bank of Canada and the Federal Reserve held their policy rates steady in January. The Bank of Canada maintained its overnight rate at 2.25%, signaling the current rate is “about right” while acknowledging heightened uncertainty around trade policy and the upcoming CUSMA renegotiation. In the United States, the Fed held the federal funds rate at 3.50–3.75% following three consecutive cuts in late 2025. Chair Powell noted the economy is expanding at a “solid pace” and indicated the Fed is “well-positioned to let the data speak.” The decision was not unanimous, with two dissenting votes favouring a further cut. Credit markets remained stable, with solid corporate fundamentals supporting spreads, though the environment continues to reward selectivity across issuers.

Commodities and Currencies

Commodities had a powerful January. Gold surged approximately 16%, setting multiple new all-time highs and closing near US$4,982 per ounce. The rally was fueled by rising U.S.–Iran tensions, central bank buying, and continued depreciation of the U.S. dollar. The pace of the move has drawn comparisons to the late 1970s, though the speed of the recent ascent has raised concerns about speculative activity, with daily volatility increasing markedly in the month’s final stretch.

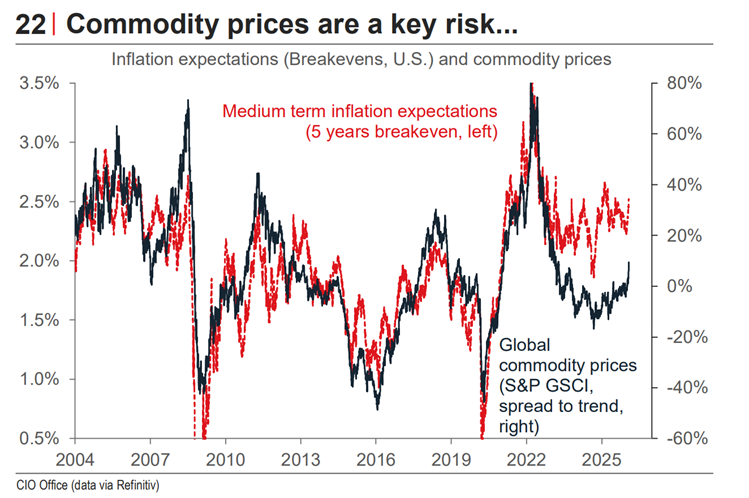

Energy prices also climbed sharply, with WTI oil rising 12.6%, driven by the prospect of U.S. military intervention in Iran and its potential impact on the Strait of Hormuz. Copper added 4.9% as the broader commodity complex showed signs of a more sustained upturn — a dynamic that poses a meaningful risk to the inflation outlook if it persists.

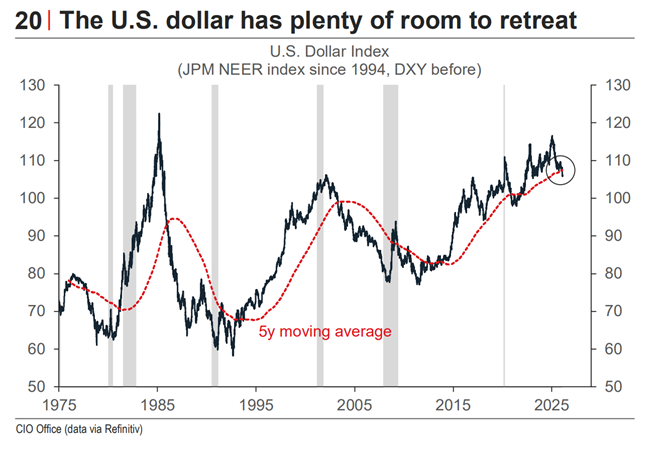

On the currency front, the U.S. dollar weakened further, with the DXY index declining 1.4%. The Greenback has now fallen approximately 10.5% from its recent peak, weighed down by unpredictable U.S. trade and economic policy. For Canadian investors, the strengthening loonie remained a headwind when translating U.S.-denominated returns, reinforcing the importance of currency management within globally diversified portfolios.

Economic Overview

US Economics:

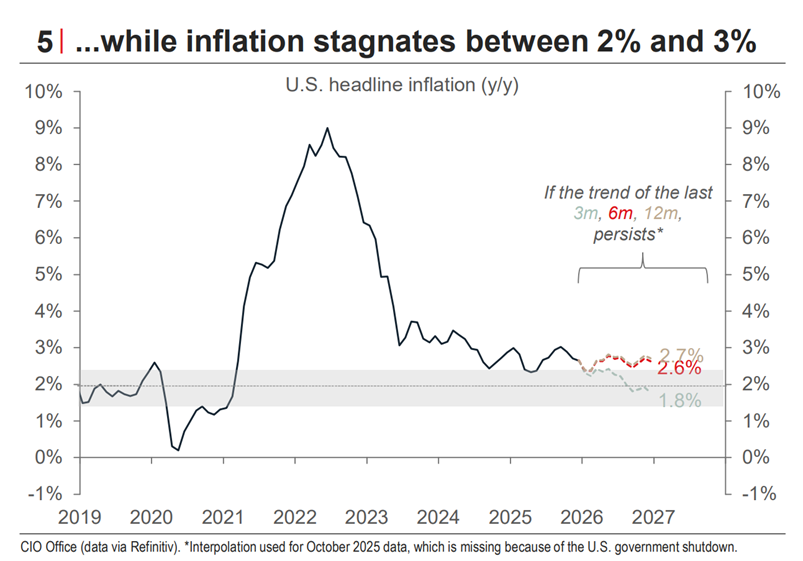

Despite an increasingly turbulent political landscape, the U.S. economy continued to deliver resilient data. The Economic Surprise Index remained in positive territory, third-quarter GDP growth was revised upward to a 4.4% annualized rate, and fourth-quarter corporate earnings are on track for the highest net profit margin in over 15 years. On inflation, headline CPI remained in the 2.5–2.7% range and wage growth moderated to the lower end of the Fed’s 3–4% comfort zone, though rising commodity prices and potential tariff pass-through represent meaningful upside risks.

Adding another layer of complexity, political pressure on the Federal Reserve escalated significantly. A Department of Justice investigation into Chair Powell was widely interpreted as an effort to influence monetary policy ahead of his term expiration in May. Powell responded firmly, framing the situation as a test of whether rate decisions would continue to be evidence-based or directed by political pressure. The nomination of Kevin Warsh as his potential successor has drawn further attention, with markets closely watching for signals about the future direction of Fed independence.

Canadian Economics:

Canada’s economic picture reflected a measured pause by policymakers. The Bank of Canada held its overnight rate at 2.25%, the second consecutive hold, with the Monetary Policy Report projecting modest GDP growth of 1.1% in 2026. CPI inflation edged to 2.4% in December, largely on base-year effects from last winter’s GST/HST holiday, while core measures continued easing toward 2.5%. The labour market presented a mixed picture — unemployment sat at 6.8% with few businesses planning to expand hiring, though layoff rates also remained low.

The dominant uncertainty for the Canadian economy remains trade policy. The formal CUSMA review, set to begin July 1, looms over business confidence. The Trump administration’s negotiating pattern — escalating threats, selective enforcement, then renegotiation — has become somewhat predictable, but no less disruptive. While midterm election dynamics may constrain more aggressive trade actions (cost of living was the top concern for 79% of Trump voters in 2024), the uncertainty itself continues to weigh on Canadian economic activity.

Bottom Line

January reinforced that we are in a period of profound transition — not in economic fundamentals, which remain broadly supportive, but in the geopolitical and policy environment that frames them. The rotation away from U.S. equity dominance intensified, the dollar continued to weaken, and gold surged to record levels as investors sought diversification from an increasingly unpredictable policy landscape. Meanwhile, corporate earnings remained strong, central banks signaled patience, and growth continued to exceed expectations.

Looking ahead, the key risks are clear: an escalation in trade tensions around the CUSMA renegotiation, a deterioration in Fed independence, and the potential for rising commodity prices to reignite inflation concerns. In this environment, we remain focused on diversification across geographies and asset classes, quality-oriented equity positioning, and disciplined portfolio construction. Markets are entering a phase where the ability to adapt to shifting leadership and manage uncertainty will be critical to delivering consistent outcomes for clients.