InsightsIran Conflict: Markets in the Fog

March 06, 2026 • 7 MIN READ

Geopolitical risk has moved sharply back into focus following the escalation of conflict involving Iran. Episodes like this tend to generate unsettling headlines, abrupt market moves, and a spike in investor anxiety. Our role is not to forecast geopolitical outcomes, but to help frame what matters most for markets and portfolios when uncertainty rises.

History reminds us that markets often react before we have full information. The challenge for investors is distinguishing between short‑term volatility driven by fear and longer‑term shifts in economic fundamentals.

1) The market’s first reaction has been classic: risk off and safe havens

When investors are confronted with sudden uncertainty, markets often move quickly and defensively. The most common initial response is risk off positioning, reduced exposure to cyclical assets, and increased demand for liquid safe havens.

This pattern has repeated itself across decades of geopolitical shocks. Initial moves can be sharp, even when the longer‑term market impact ultimately fades. The early phase is dominated by positioning, hedging, and uncertainty rather than fundamental reassessment.

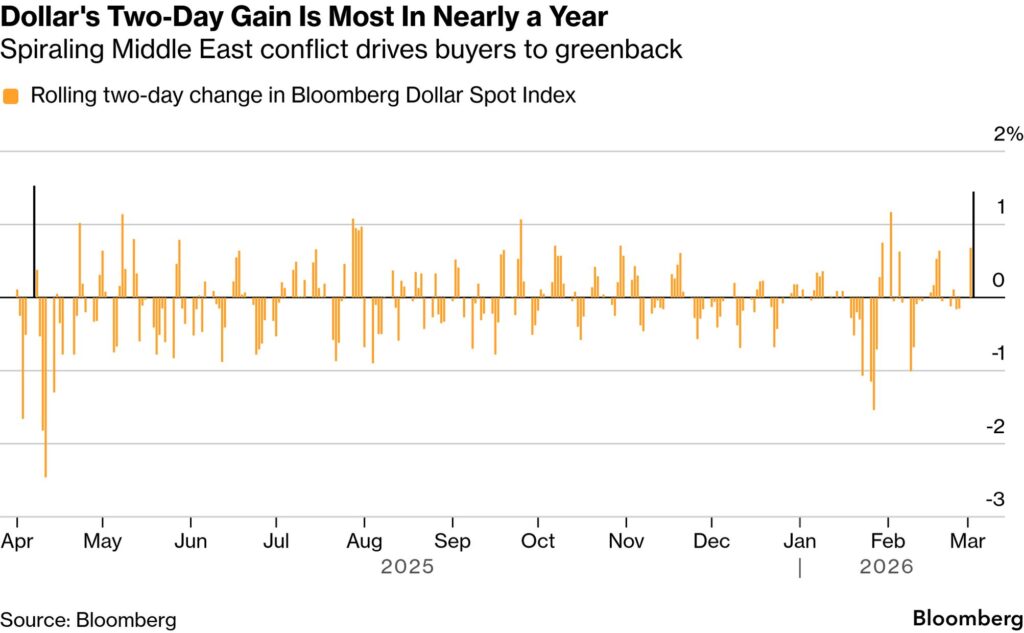

The chart included above shows a bar series titled “Dollar’s Two‑Day Gain Is Most in Nearly a Year”, illustrating rolling two‑day changes in the Bloomberg Dollar Spot Index. The largest bars approach the upper end of the range, highlighting how quickly demand for the US dollar surged as Middle East tensions escalated.

This is a textbook example of a flight to liquidity. When uncertainty rises, the US dollar often strengthens because it remains the world’s deepest reserve currency market and because deleveraging and hedging flows can create short‑term demand for dollars. While currency moves can reverse quickly, the signal is not about predicting the dollar. It is about recognizing elevated near‑term uncertainty.

2) The key transmission mechanism is not the headlines, it is energy and shipping

There are countless geopolitical narratives, but markets tend to respond through a limited set of measurable economic channels. In this episode, the dominant pathway runs through energy.

• Conflict escalation increases perceived risk

• Shipping and insurance costs rise

• Energy supply becomes less certain

• Oil prices move higher

• Inflation risks increase

• Central banks face tighter constraints

• Earnings and valuations come under pressure

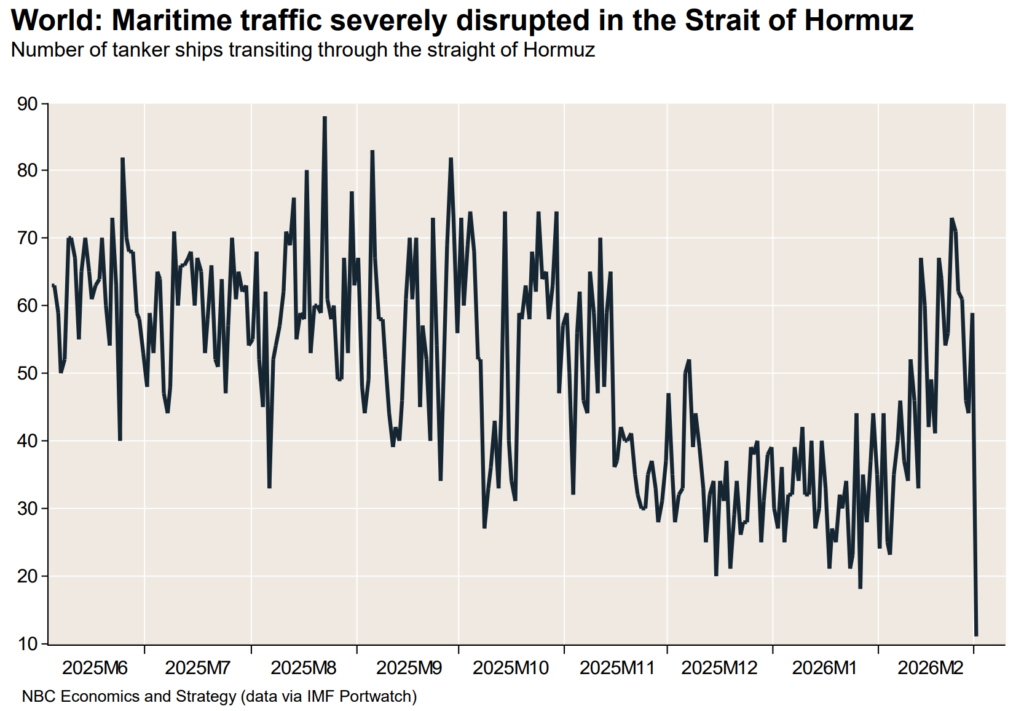

Disruption around the Strait of Hormuz is central to this dynamic. Shipping activity has slowed, insurers have repriced risk, and energy markets are embedding a higher geopolitical premium. Importantly, energy prices can rise sharply even without widespread physical damage to oil infrastructure.

In the early stages of conflict, logistics matter as much as production. Shipping flows, insurance availability, and risk premia embedded in futures markets can effectively tighten supply even if production sites remain intact.

Why the Strait of Hormuz matters in plain English

The Strait of Hormuz is one of the world’s most important maritime chokepoints for oil and liquefied natural gas. When traffic slows, insurance is withdrawn, or shipping routes become more expensive or risky, less energy reaches end markets. That can lift crude prices, refined product prices, and inflation expectations even before physical shortages appear.

3) The most important question for markets: does this become an inflation shock

Markets can look through geopolitical events surprisingly well unless those events trigger a persistent macroeconomic change. Historically, the differentiator has been whether the shock feeds through to inflation, interest rates, and growth.

If energy prices remain elevated for long enough, inflation risks rise. That limits the ability of central banks to ease policy and can keep interest rates higher for longer. Because discount rates and earnings expectations sit at the core of equity valuations, this channel matters far more than the headlines themselves.

A simple three‑scenario framework

We think about environments like this in scenarios, not predictions.

• Scenario A: Contained

Shipping conditions normalize, oil stabilizes, volatility fades, and markets refocus on fundamentals.

• Scenario B: Drag

Disruption persists for weeks or months. Energy prices remain elevated. Inflation progress stalls. Markets experience extended volatility and leadership rotation rather than a clear trend.

• Scenario C: Shock

Energy flows are materially constrained for a sustained period. Oil prices spike. Inflation reaccelerates. Growth slows meaningfully and recession risk rises.

Markets typically oscillate between the first two scenarios. The third is what investors fear most and what markets briefly price during volatility spikes, but it requires persistent second‑round inflation effects.

4) What history says: markets often recover faster than headlines suggest

One of the most consistent lessons from market history is that geopolitical shocks rarely dictate long‑term outcomes on their own. While short‑term drawdowns can be uncomfortable, markets have often stabilized and recovered within a relatively short window when economic fundamentals remain intact.

This is not a promise of an immediate rebound. It is a reminder that the emotional intensity of a headline is often disproportionate to its long‑term impact on diversified portfolios. Markets are forward‑looking and tend to reprice risk quickly once uncertainty becomes known rather than unknown.

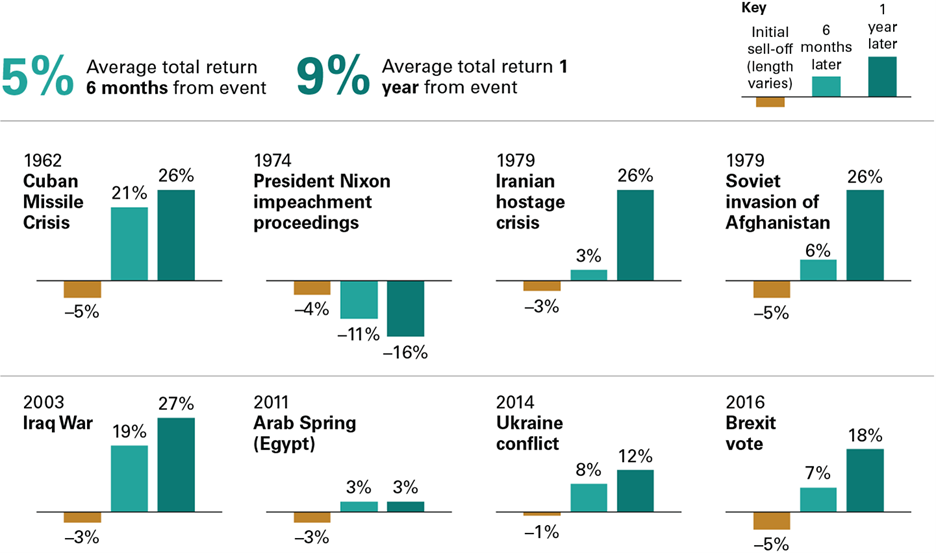

Just look at past events as evidence. This chart ” Markets Historically Recover After Geopolitical Shocks”

This chart shows that while major geopolitical or political events often trigger short‑term market declines, stock markets have historically rebounded strongly within six months to one year. On average, returns turn positive fairly quickly, with about 5% gains after six months and 9% gains after one year, highlighting the market’s resilience after periods of crisis.

5) Sector and regional implications: dispersion rises when energy leads

When energy is the primary transmission mechanism, market leadership tends to rotate rather than disappear.

• Energy and materials can benefit from higher commodity prices

• Energy‑intensive industries face margin pressure

• Consumer‑sensitive sectors may struggle as costs rise

• Commodity‑linked regions can outperform major energy importers

Rising energy prices can also complicate the inflation path, influencing bond yields and central bank policy. When yields rise for inflation reasons, market leadership can shift away from long‑duration assets toward cash‑flow‑oriented or real‑asset‑linked exposures.

An important nuance is that we do not build portfolios around short‑term geopolitical or war‑related trades. The objective is not to gamble on outcomes, but to maintain alignment with long‑term goals while managing risk prudently.

6) What we are watching closely

Rather than reacting to daily headlines, we focus on indicators that historically matter most.

• Shipping and insurance conditions around the Strait of Hormuz

• Oil prices and the structure of the futures curve

• Inflation expectations and longer‑term bond yields

• Credit spreads as a signal of financial stress

• Equity market breadth and leadership

These data points help determine whether geopolitical risk is translating into lasting economic pressure or remaining a volatility event.

7) How we manage portfolios during periods like this

Periods of elevated uncertainty are when discipline matters most.

We avoid large reactive shifts based on incomplete information. History shows that selling into volatility and re‑entering after markets stabilize often undermines long‑term results.

Instead, we remain anchored to portfolios built around long‑term objectives, time horizons, and risk tolerance. Volatility can create opportunities for systematic rebalancing, allowing portfolios to realign with targets without relying on predictions.

We continue to monitor whether higher energy prices materially affect inflation expectations, interest rates, or credit conditions. If fundamentals change, we adapt. Until then, process matters more than prediction.

Bottom line

The situation remains fluid, and uncertainty is elevated. Markets are responding primarily through the energy and inflation channel rather than panic.

If disruptions remain contained, history suggests markets can regain their footing. If inflation pressures persist, volatility may last longer and leadership may rotate, but disciplined portfolios are built for these environments.

As always, portfolios are designed around long‑term goals, not short‑term headlines. We remain focused on the signals that matter and available to discuss how this environment fits into your broader plan.

Sources

AdvisorAnalyst and LPL Financial

Iran Escalation How Markets Have Reacted to Geopolitical Events

March 4, 2026

BMO ETFs

Weekly Basis Points Iran Conflict Six Points to Make

March 1, 2026

National Bank Financial

Geopolitical Briefing Iran Conflict Trying to See Through the Fog of War

March 3, 2026

Reuters

Iran spent years fostering proxies in Iraq. Now, many aren’t eager to join the war

March 6, 2026