InsightsMonthly Market Wrap – March 2026

April 07, 2026 • 7 MIN READ

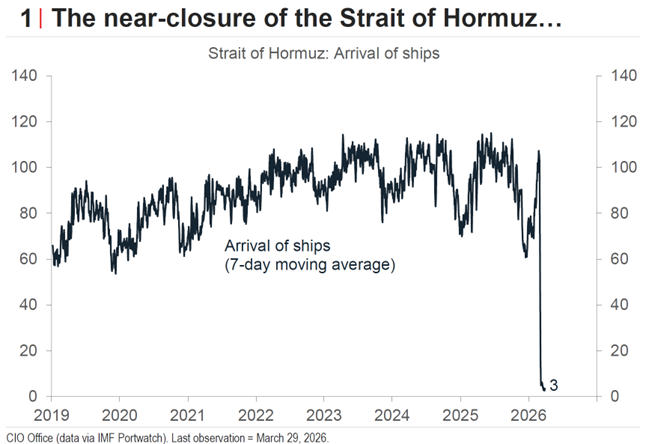

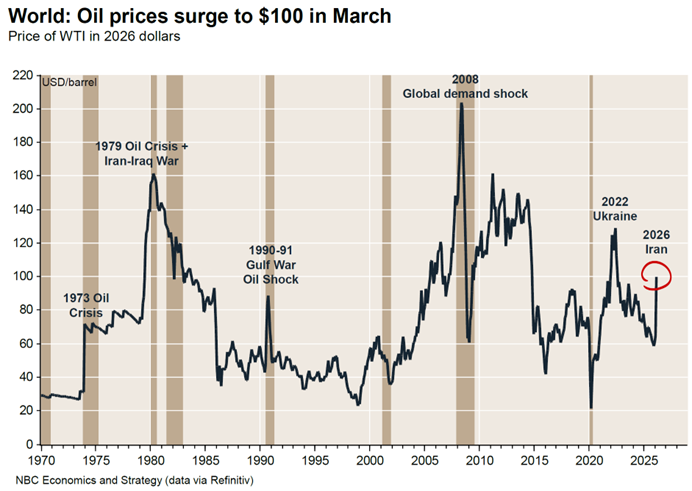

March 2026 brought a sharp reversal in global markets as geopolitical shock overtook economic momentum. The United States and Israel launched military strikes against Iran on February 28th, triggering a near-complete closure of the Strait of Hormuz and sending crude oil prices above $100 per barrel for the first time since 2022. Global equities sold off broadly, though the Canadian market demonstrated meaningful resilience given its commodity weighting and net energy-exporter status. The path ahead depends heavily on the duration of the conflict, central bank responses to a renewed inflation threat, and whether global economic growth can absorb a sustained supply disruption.

Equity Markets

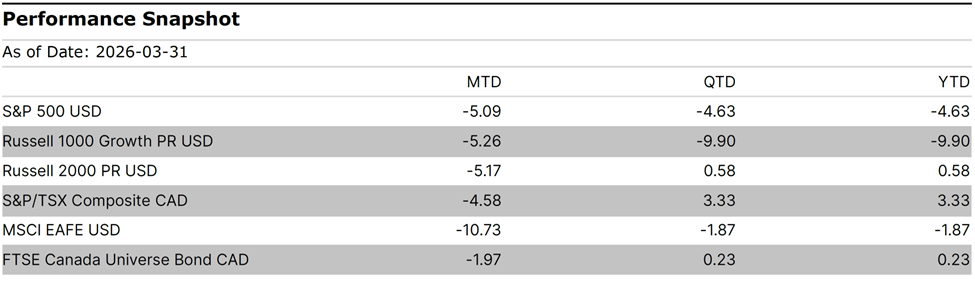

The S&P 500 declined approximately 5.1% in March, bringing its year-to-date return to −4.6% — a performance eerily similar to the early months of 2022, though the sectoral backdrop appears more fragile this time around. Financials fell roughly 11.0% year-to-date and Consumer Discretionary declined approximately 10.6%, while even the Technology sector (carrying outsized index weight) is down approximately 8.5% on the year.

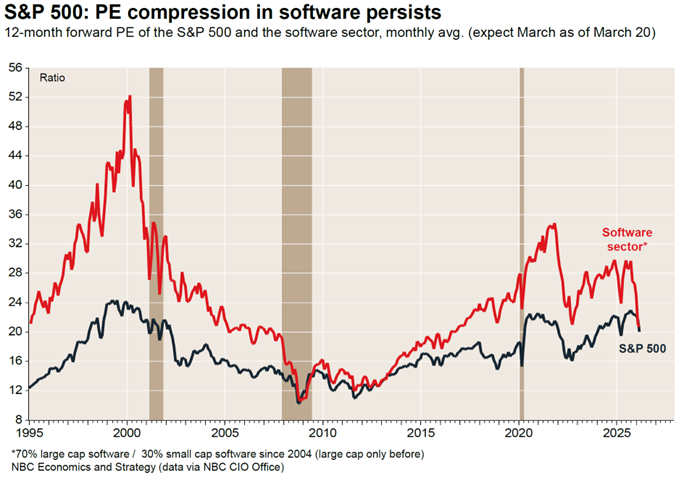

Beneath the surface, the software sector is experiencing what can only be described as a bear market in its own right, as fears that artificial intelligence will erode the competitive moats of incumbent technology platforms have triggered one of the most significant drawdowns the sector has seen outside of a broader recession. While the S&P 500 is down approximately 5%, that headline figure obscures the damage underneath. Microsoft, for example, has declined more than 20% year-to-date, a stark reminder that index-level returns can mask severe dislocations in individual names.

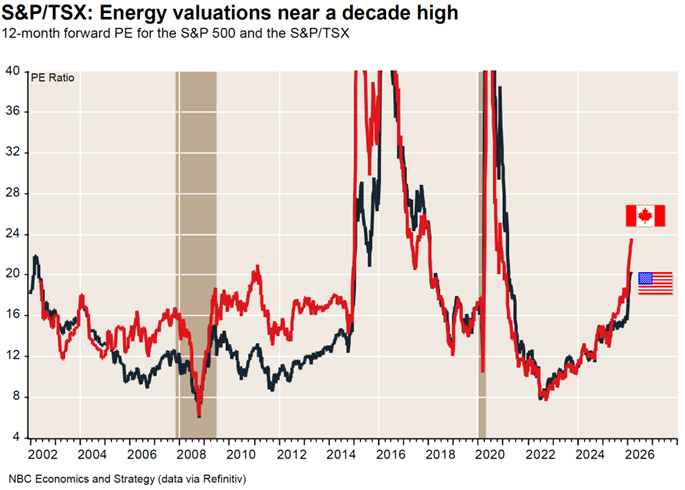

Canadian equities demonstrated relative resilience, with the S&P/TSX Composite declining 4.6% for the month but remaining positive year-to-date at +3.3%. The pattern mirrors 2022, when Canada’s heavier commodity weighting and lighter technology exposure insulated the TSX from the worst of the U.S. selloff. Energy sector valuations have climbed to 24 times forward earnings (well above historical averages) and Canadian energy stocks are now trading at roughly a 20% premium to their U.S. counterparts for the first time in over a decade.

International equities bore the heaviest losses, with the MSCI EAFE declining approximately 10.7% in March. Europe’s acute vulnerability to Middle Eastern energy supply disruptions weighed on sentiment, and the euro surrendered its early-2026 gains as stagflationary pressures mounted. Looking ahead, consensus EPS growth expectations of approximately 18% for global equities in 2026 remain ambitious, and the energy-driven cost squeeze on corporate margins means downward revisions are likely as the conflict’s duration becomes clearer.

Fixed Income and Credit

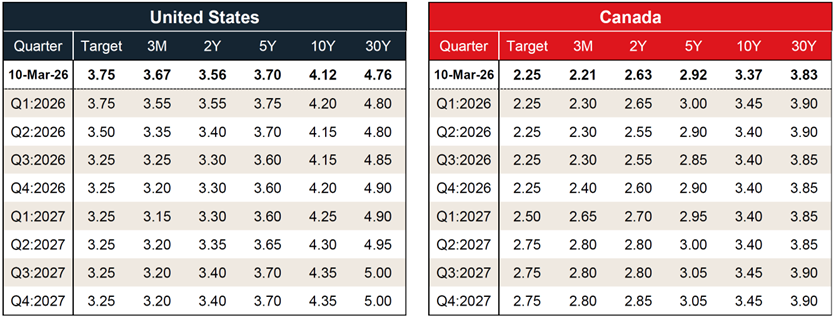

Bond markets experienced significant volatility in March, with the FTSE Canada Universe Bond Index declining 1.97% for the month, though it remains marginally positive year-to-date at +0.23%. The competing forces of safe-haven demand and oil-driven inflation complicated the outlook for both central banks. The Federal Reserve held its policy rate at 3.75% and the Bank of Canada remained on hold at 2.25%, with both institutions navigating the difficult trade-off between softening labour markets and renewed upward pressure on headline inflation.

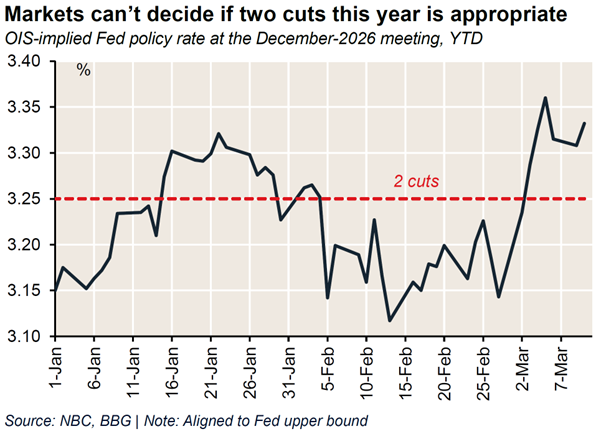

The path to further rate cuts has narrowed materially. U.S. 10-year yields stood near 4.12% at mid-month, with 30-year yields approaching 4.76%, and markets have dialled back from pricing three Federal Reserve cuts in 2026 to debating whether two remain achievable.

In Canada, the Bank has signalled that headline inflation will be its guiding light in the months ahead, even as it looks through the near-term energy-price surge. Corporate credit has remained broadly stable, though the tightening of financial conditions warrants continued selectivity in favour of higher-quality issuers.

Commodities and Currencies

The surge in crude oil prices was the defining commodity move of the month. WTI climbed to approximately $100 per barrel in March and continued higher into early April, reflecting what the IEA has characterised as the largest oil supply disruption in market history.

The Canadian dollar proved to be one of the strongest-performing major currencies since the onset of the Iran conflict, supported by Canada’s position as the G7’s largest net energy exporter relative to GDP — approximately 4.4% of nominal GDP.

The broad U.S. Dollar Index rebounded approximately 2% from its recent lows on geopolitical safe-haven demand, though the structural case for sustained dollar strength is considerably weaker than it was at the onset of the 2022 oil shock, with inflation and policy rates already near neutral rather than deeply accommodative.

Economic Overview

United States

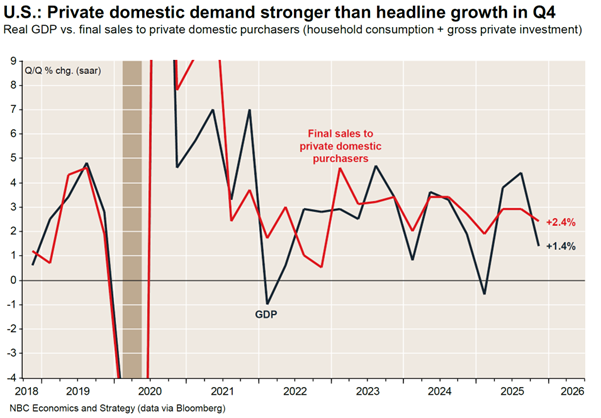

The U.S. economy entered this period of geopolitical uncertainty in reasonably good shape. Fourth-quarter 2025 GDP growth of 1.4% annualised disappointed consensus expectations of 2.8%, though the shortfall was largely attributable to the longest government shutdown in U.S. history, which subtracted 1.15 percentage points from annualised growth. Stripping out that impact, final sales to private domestic purchasers grew at a healthier 2.4% annualised rate, and AI-driven capital expenditure remains a constructive force, with investment in information-processing equipment up 28.1% on an annual basis.

Labour market data has been more mixed. February saw a sharp decline of 86,000 in private payrolls, the largest single-month drop since late 2020, and the unemployment rate has risen to 4.4%. Core inflation remains above the Fed’s 2% target, with CPI running near 2.5% and PCE closer to 3.1%, leaving limited room for aggressive easing even as growth moderates. The baseline GDP forecast for 2026 has been revised to 2.5%, with the acknowledged risk that a prolonged Strait of Hormuz disruption could materially alter that trajectory.

Canada

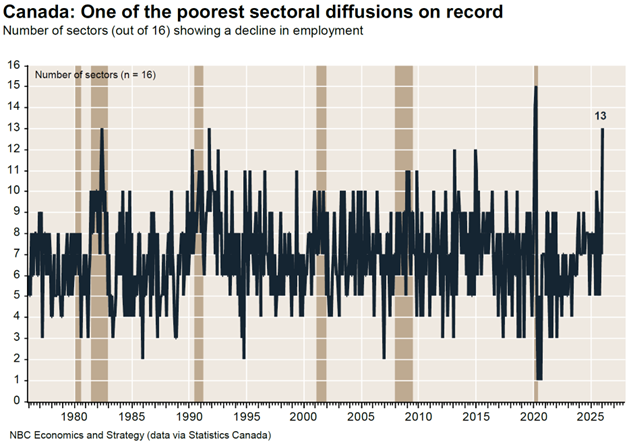

Canada’s economic outlook has become more challenging, layering a geopolitical shock on top of already fragile domestic conditions. The GDP growth forecast for 2026 has been revised down to 0.9%, as the economy closed 2025 with its second contraction in three quarters. February’s employment report was particularly alarming: the economy shed 84,000 jobs, following a loss of 25,000 in January, with 13 of 16 sectors contracting; a breadth of weakness that ranks among the worst readings in nearly 600 months of data.

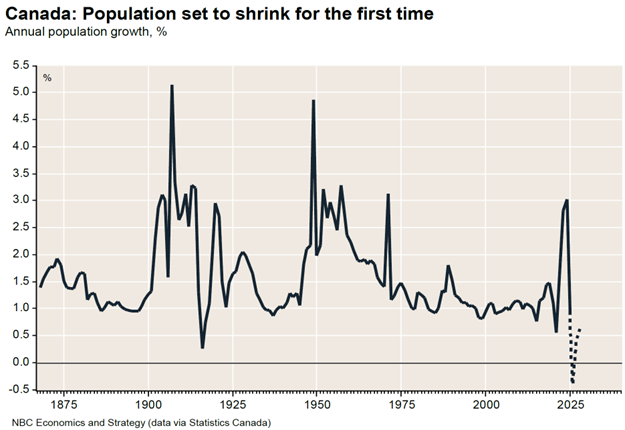

The Bank of Canada remains on hold at 2.25% and is expected to stay there throughout 2026, balancing a fragile economy against an inflation outlook now projected at approximately 2.5% for the year. Population growth has effectively been shut off, with 2025 marking the first annual population decline since Confederation, a headwind for housing demand and consumer activity that will persist. Canada’s net energy-exporter status provides some offset, and a favourable resolution to the CUSMA negotiations could offer a meaningful tailwind to activity in the second half of the year.

Bottom Line

March 2026 was defined by a geopolitical shock that arrived at an already complex moment for markets. The Iran conflict and the oil surge it triggered reordered sector leadership, complicated the inflation and rate-cut outlook for both the Fed and the Bank of Canada, and introduced a level of macro uncertainty not seen since the early months of 2022. Canadian markets held up better than most, reflecting structural advantages that are likely to persist as long as oil prices remain elevated.

The risks ahead are meaningful. A prolonged disruption to Strait of Hormuz shipping carries escalating consequences for global growth and corporate earnings. History offers little comfort, as major oil shocks have typically coincided with equity bear markets. Valuations in the U.S. remain elevated, CUSMA negotiations this summer add a further layer of trade policy uncertainty, and Canada’s demographic contraction presents a structural challenge with no near-term resolution.

In this environment, we remain focused on maintaining diversification, emphasising quality investments, and preserving the flexibility to respond as conditions evolve. This is a period that calls for discipline and patience rather than reactivity and the same measured, long-term approach that has served clients well through prior cycles of uncertainty remains the appropriate posture today.