InsightsMonthly Market Wrap – February 2026

March 06, 2026 • 6 MIN READ

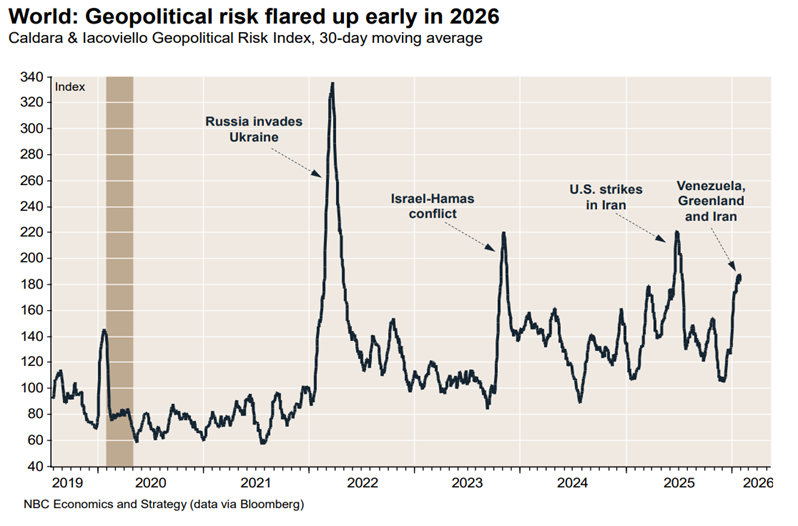

Global markets continued their strong start to 2026, building on the powerful rally seen in 2025. Despite growing geopolitical tensions and the expansion of protectionist trade policies, equity markets have remained resilient. Investors appear increasingly focused on earnings growth expectations and supportive financial conditions rather than trade frictions. While market leadership has begun to broaden beyond the large technology companies that dominated the previous cycle, elevated valuations and shifting macro conditions continue to suggest a more balanced and potentially volatile environment ahead.

Equity Markets

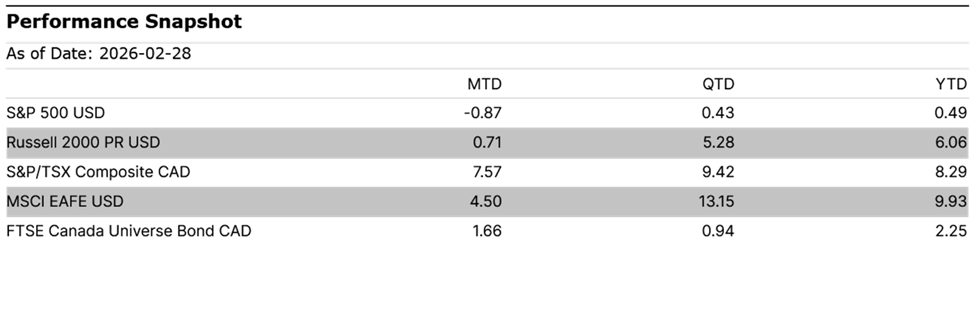

Global equity markets posted modest gains through February, although performance across regions and sectors was uneven. The S&P 500 experienced a sluggish start to the year, largely reflecting weakness within the information technology sector following its exceptional performance in 2025. Concerns have emerged that the scale of capital expenditures required to support artificial intelligence infrastructure could pressure profitability in parts of the software and technology ecosystem.

At the same time, more traditional sectors of the economy have shown improving momentum. Industrials, energy, and materials have outperformed early in the year, supported by government initiatives aimed at strengthening domestic manufacturing capacity and rebuilding supply chains. These sectors also stand to benefit from rising infrastructure investment and increasing demand for electricity and industrial metals tied to the rapid expansion of digital infrastructure and electrification.

Canadian equities have also started the year on a constructive footing following their exceptional performance in 2025. The S&P/TSX delivered one of the strongest returns among developed markets last year, driven largely by strong performance from gold producers and other resource-oriented sectors. While commodity strength may continue to support Canadian markets, emerging demographic headwinds—including Canada’s first population decline in modern history—could weigh on more consumer-oriented sectors of the economy.

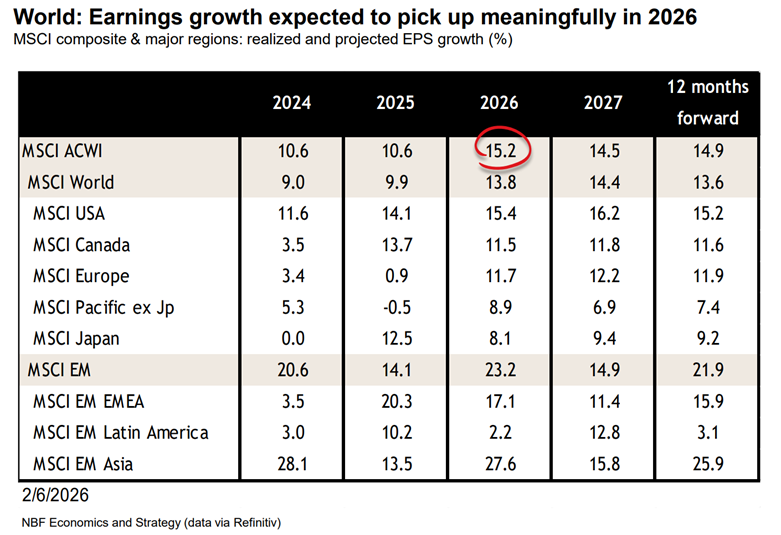

Globally, earnings expectations remain optimistic. Consensus forecasts suggest global earnings growth could accelerate in 2026, driven by productivity gains from technological adoption, fiscal stimulus across several regions, and stronger commodity prices. However, these projections leave limited room for disappointment should economic growth slow or profit margins fail to expand as expected.

Fixed Income and Credit

Fixed income markets were relatively stable through February as investors continued to reassess the trajectory of monetary policy. After an extended period of rate cuts across developed markets in 2025, central banks appear to be approaching the limits of their easing cycles.

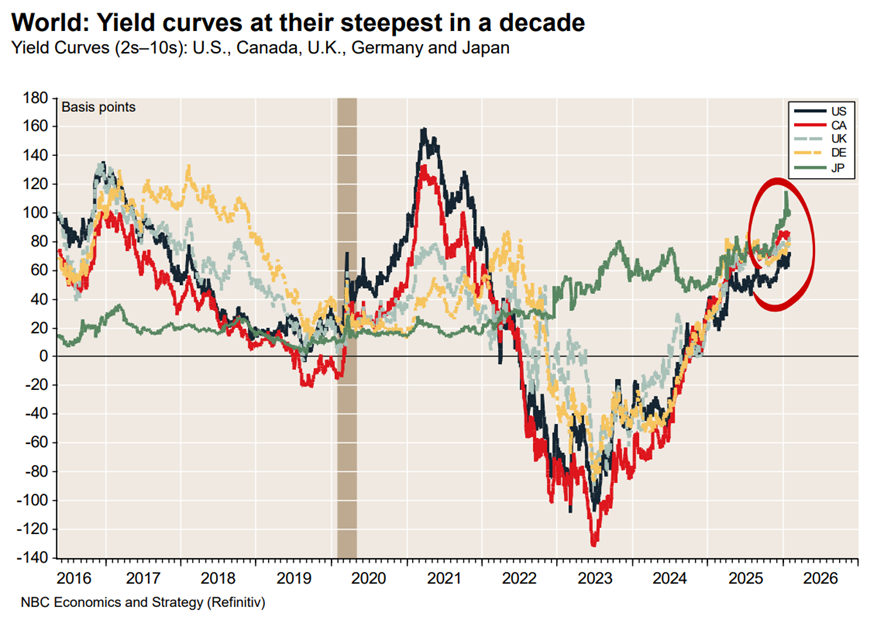

Yield curves across major economies have steepened to their highest levels in more than a decade, reflecting expectations that policy rates may decline modestly while longer-term growth and inflation expectations remain elevated. This dynamic has contributed to increased volatility in bond markets but has also improved income opportunities for fixed income investors.

Credit markets remain broadly constructive. Corporate balance sheets are generally healthy and default rates remain low. However, investors have become increasingly selective, with greater differentiation emerging between higher-quality issuers and more leveraged borrowers. In this environment, a disciplined approach emphasizing credit quality and income sustainability remains particularly important.

Commodities and Currencies

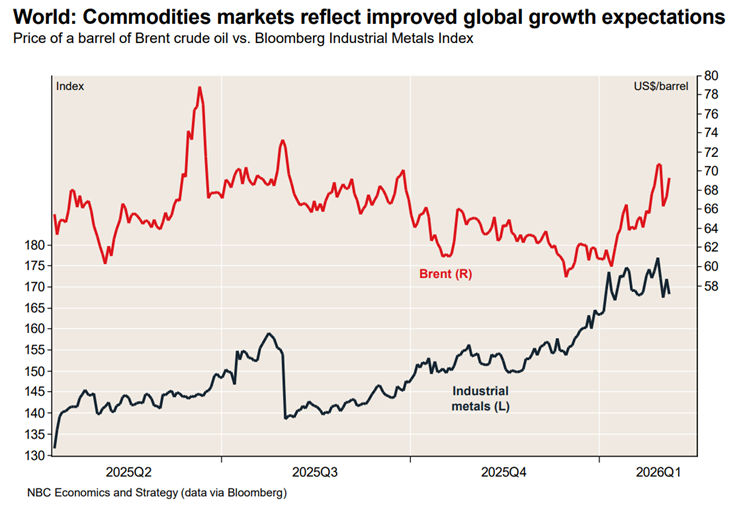

Commodity markets continued to play an important role in shaping equity performance early in 2026. Industrial metals and energy-related sectors have benefited from the prospect of increased infrastructure spending and rising electricity demand associated with data centres, electrification, and the expansion of artificial intelligence infrastructure.

Currency markets were relatively stable during the month. However, the broader trend observed in 2025 remains an important consideration for Canadian investors. The U.S. dollar experienced notable weakness against the Canadian dollar over the past year, which reduced the Canadian-dollar returns of U.S. investments despite strong underlying equity performance. As a result, currency translation effects understated the performance of many globally diversified portfolios.

Economic Overview

United States

The U.S. economy continues to demonstrate remarkable resilience despite a challenging political and policy environment. Fourth-quarter economic data remained solid even as the country experienced the longest federal government shutdown in its history, which forced hundreds of thousands of government employees to take unpaid leave. The limited economic impact of this disruption highlights the underlying strength of domestic demand.

Business investment remains a key driver of growth, particularly in equipment spending tied to the rapid development of artificial intelligence infrastructure. Major technology firms are expected to increase their capital expenditures on AI-related investments to roughly $650 billion in 2026, providing a significant boost to economic activity.

Consumer spending has also remained relatively resilient, though there are emerging signs of moderation. Household spending has been growing faster than disposable income over the past year, pushing the savings rate to its lowest level since the pre-financial-crisis period. While this dynamic may eventually slow consumption growth, strong labour market participation and favourable financial conditions continue to support the broader economic expansion.

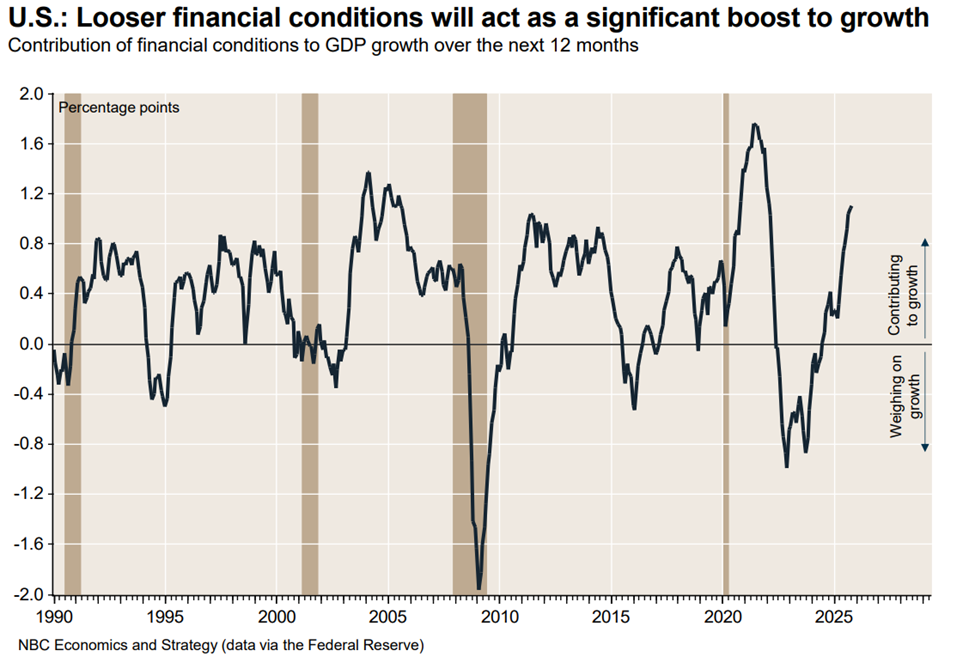

Looking ahead, the United States is expected to maintain solid economic growth in 2026. Although inflation may remain above the Federal Reserve’s target for longer than markets anticipate, looser financial conditions can acts also as a significant boost to growth.

Canada

Canada’s economic outlook remains more challenging. Trade tensions with the United States have intensified at a time when the renewal of the USMCA trade agreement is approaching, creating additional uncertainty for businesses and investors.

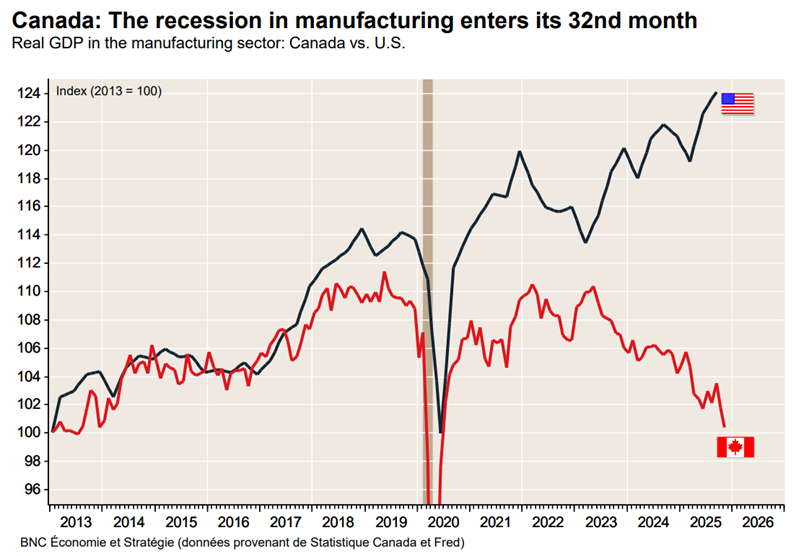

The Canadian manufacturing sector has been particularly weak, experiencing its longest recession in at least a generation. Activity in the sector has declined steadily since 2023 and now sits at its lowest level since 2013 outside of the pandemic period. This weakness reflects both external factors—including U.S. protectionist policies—and domestic policy challenges that have discouraged industrial investment.

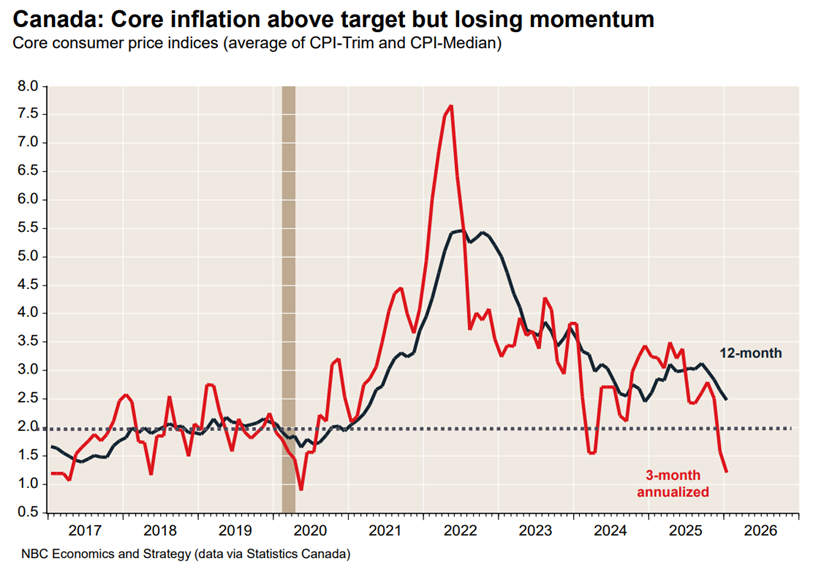

Despite these headwinds, the labour market has shown surprising resilience. The unemployment rate declined earlier this year as labour force participation fell sharply, although this improvement may prove temporary as participation rates normalize. At the same time, wage growth has moderated significantly, helping ease inflationary pressures and providing the Bank of Canada with greater flexibility should economic conditions deteriorate.

Nevertheless, economic growth expectations have been revised slightly lower. Canadian GDP is now expected to expand by approximately 1.1% in 2026, reflecting weaker population growth and ongoing uncertainty surrounding trade policy and investment conditions.

Bottom Line

Markets have entered 2026 with considerable momentum, supported by resilient economic growth, strong corporate earnings expectations, and supportive financial conditions. However, the investment environment remains complex.

Equity valuations remain elevated, and market leadership continues to shift as investors reassess the sustainability of the previous cycle’s technology-driven gains. At the same time, geopolitical tensions, protectionist trade policies, and uncertain fiscal trajectories could introduce additional volatility in the months ahead.

While the global economy—particularly the United States—continues to show resilience, strong economic conditions do not eliminate the possibility of market corrections. As a result, maintaining diversification, emphasizing quality investments, and preserving flexibility within portfolios remain essential as markets navigate the next phase of the economic cycle.