InsightsFrom Chatbots to Coworkers: How AI Is Rewriting the Rules of Enterprise Software

April 07, 2026 • 7 MIN READ

The competitive moat of enterprise software is being stress-tested. Here is what investors need to understand.

Not long ago, artificial intelligence in enterprise software was mostly a feature. A smarter search bar. A grammar assistant. A way to auto-fill a form. Software companies added “AI-powered” to their marketing, and Wall Street rewarded them for it. That story has changed quickly.

What is happening now is more significant. AI is no longer just helping workers get things done faster. In many cases, it is doing the work itself. The latest models from Anthropic and OpenAI can now complete tasks autonomously that once took a skilled employee an hour or more. This shift from AI as a tool to AI as a worker is forcing a real rethink of how enterprise software is valued, priced, and used.

The data is already in the charts

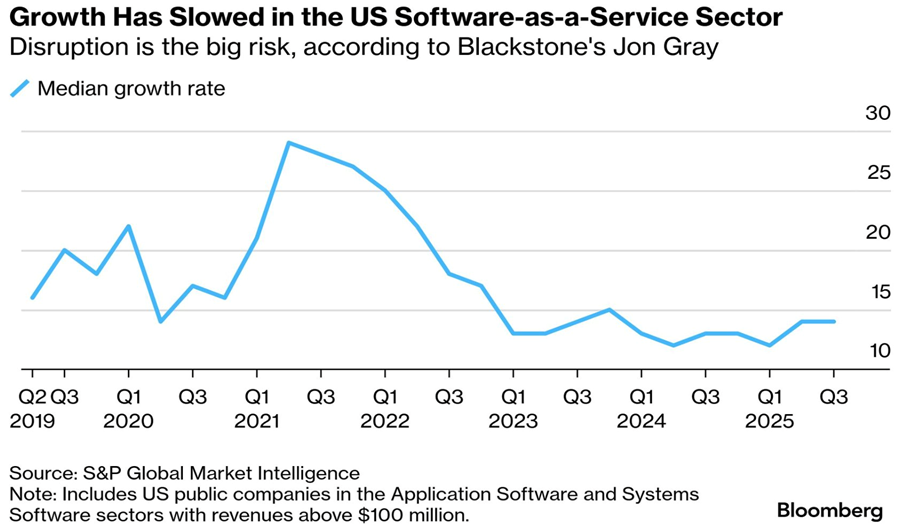

The slowdown in software growth started before AI disruption became the main story. Revenue growth across large US public software companies peaked near 27% in mid-2021, driven by a surge in digital spending during the pandemic. By late 2025, that figure had fallen to around 12%, closer to where it was before the cloud software boom began.

Median revenue growth for US public software companies with revenues above $100M. Source: S&P Global Market Intelligence via Bloomberg.

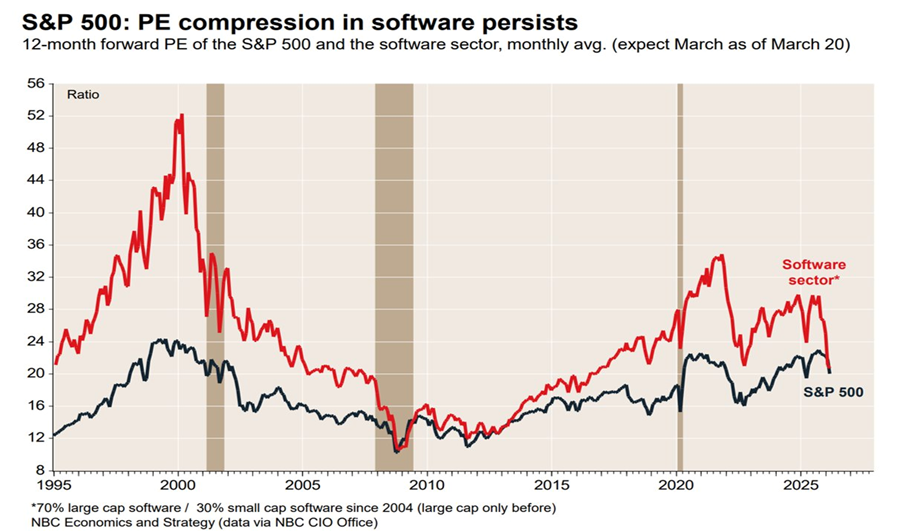

Making things harder, investors are also paying less for that slower growth. The forward price-to-earnings ratio for software stocks, which surged above 35x in 2021, has been falling steadily. Today, software trades at roughly the same premium over the broader market as it did in the mid-2010s, well before the SaaS boom pushed valuations to historic highs.

12-month forward PE of the S&P 500 vs. the software sector, monthly average. Source: NBC Economics & Strategy / NBC CIO Office.

Slower growth and lower multiples together created the conditions for what Wall Street has started calling the “SaaSpocalypse.” In early February 2026, roughly $300 billion in market value disappeared from the software sector in less than 48 hours. Earnings misses, cautious guidance from corporate IT departments, and a warning from Morgan Stanley about stress in the $235 billion software loan market all hit at once. Nearly half of that debt carries a below-investment-grade credit rating, raising the prospect of defaults if revenue keeps slowing.

AI can now complete real tasks, not just assist with them

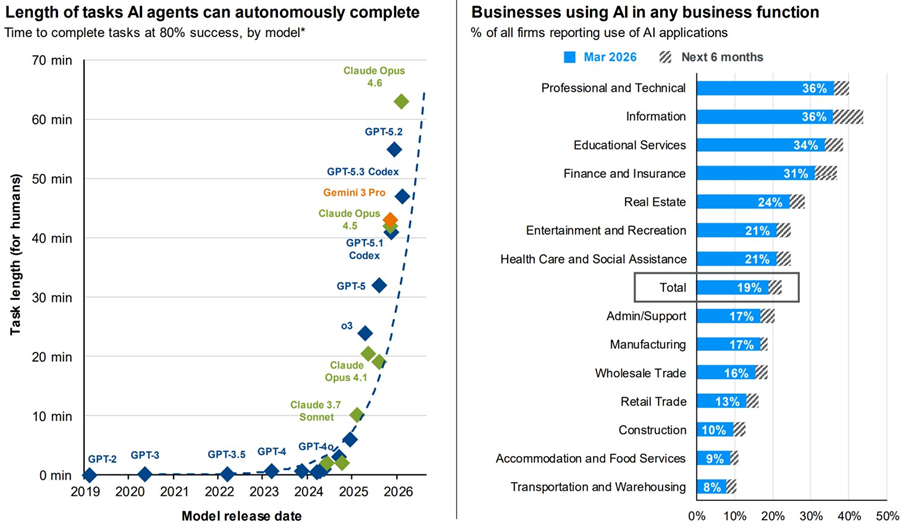

The chart below helps explain why investors are so unsettled. It tracks how long a task AI models can complete on their own, measured by achieving an 80% success rate. Just a few years ago, that number was close to zero. By early 2026, Anthropic’s Claude Opus 4.6 model is past 60 minutes, with the curve still rising steeply.

Left: Autonomous task duration by model at 80% success rate. Right: Share of businesses using AI by sector. Source: Morgan Stanley.

This progression matters because most enterprise software is priced by the number of people using it. Salesforce charges per sales rep. Legal research tools charge per attorney. Project management software scales with team size. If an AI agent can do the work of five, ten, or twenty of those users, companies will naturally question whether they need as many seats. That is a direct threat to the revenue model that has powered the software industry for two decades.

We are already seeing this play out. In early 2026, legal software stocks dropped sharply after Anthropic released tools capable of automating complex legal research and drafting. Adobe, Salesforce, and Intuit have all seen material selloffs as investors start to rethink how many human seats these platforms will need to support five years from now.

AI is no longer just helping workers get things done faster. In many cases, it is doing the work itself.

Is the competitive moat still intact?

For a long time, the investment case for enterprise software rested on one core idea: switching costs. Once a large company had built its operations around a platform like Salesforce or Workday, moving to something else was painful and expensive. Data migration, retraining staff, rebuilding integrations meant the hassle kept customers in place, and that stickiness made for very reliable recurring revenue.

That advantage has not disappeared. But it is being looked at much more closely. The question investors are now asking is not just whether a competitor can build a better product, but whether an AI agent can simply replicate what the product does without anyone needing to buy it. For simpler, more focused software tools, the answer is increasingly yes.

That said, replacing core business systems at a large enterprise is a very different challenge. Swapping out a healthcare information system, a core banking platform, or a major ERP is not primarily a technology problem. It is a compliance problem, a security problem, and a change management problem. The time, cost, and risk involved means large enterprises tend to stay put, even when alternatives exist. That reality provides a degree of protection for the major platforms that the current headlines sometimes obscure.

The pricing model has to change

Even if the major platforms retain their customers, the way they charge them will likely need to evolve. Seat-based pricing, where revenue grows as a company adds more users, works well when humans are doing the work. It works less well when AI agents are handling an increasing share of the tasks.

The natural alternative is usage-based or outcome-based pricing, where customers pay for what gets done rather than how many accounts are active. Several companies are already moving in this direction. Salesforce’s Agentforce, ServiceNow’s AI workflow tools, and Microsoft’s Copilot expansion are all attempts to capture the value of AI within existing customer relationships, rather than let that value flow elsewhere. The transition is not painless, and it creates revenue uncertainty in the near term. But companies that get it right may end up with a more durable business than the seat model ever offered.

Consolidation, not collapse

It is worth remembering that technology has disrupted software before. The move from desktop software to cloud computing reshaped the entire industry. So did the rise of mobile. In both cases, some companies were displaced, but the overall size and value of the software market grew. The pattern tends to follow a similar path: disruption accelerates consolidation, and the companies with the strongest customer relationships and the broadest platforms tend to come out ahead.

The same logic applies here. Narrow, single-purpose software tools are most at risk. Broader platforms that sit at the centre of how businesses operate are better placed to absorb AI capabilities and hold onto their customers. Companies like ServiceNow and Oracle, which serve as essential infrastructure for large enterprises, are increasingly seen as consolidation beneficiaries rather than casualties.

The current selloff has also created some genuine valuation opportunities. Software price-to-sales ratios have compressed from around 9x to 6x, levels not seen since the mid-2010s. For investors willing to look past the near-term noise and focus on which companies have the customer depth and platform breadth to adapt, the dislocation may be meaningful.

The Verus view

Disruption is not the same as extinction. The software sector is facing real and accelerating change, and the repricing of growth multiples reflects a legitimate reassessment of what the future looks like. But software is not going away. It is changing, and the companies that update their pricing models, protect their data advantages, and treat AI as an opportunity rather than a threat are likely to define the next era of enterprise technology.

At Verus Financial, we are following these developments closely, particularly as they affect the technology positions in our managed portfolios. The companies we are most focused on share a few common traits: deep integration into their customers’ operations, enough breadth to benefit from industry consolidation, and management teams that are actively adapting rather than waiting to see what happens.

The headlines about a SaaSpocalypse are dramatic. But so is the opportunity that tends to follow any major disruption, for investors who take the time to separate the companies that will adapt from those that will not.

SOURCES & FURTHER READING

• Forbes — SaaSpocalypse Now: AI Is Disrupting SaaS, But Not All Software Is Doomed

• Bain & Company — Why SaaS Stocks Have Dropped and What It Signals for Software’s Next Chapter

• MarketMinute — SaaSpocalypse 2026: Why Wall Street Is Slashing Software Valuations

• Bloomberg — Legal Software Stocks Plunge as Anthropic Releases New AI Tool