InsightsMonthly Market Wrap – April 2026

May 11, 2026 • 8 MIN READ

Global equity markets staged a powerful rebound in April, recovering decisively from March’s weakness as a ceasefire between the United States and Iran restored risk appetite and the renewed enthusiasm for artificial intelligence reasserted itself. The MSCI ACWI advanced 10.2% in U.S. dollar terms, with Emerging Markets and the United States leading the recovery while Canada lagged the rest of the world. Beneath the headline relief, however, the situation remains complex: oil prices still hover near $100 per barrel, the Strait of Hormuz remains effectively shut, and resilient earnings growth must now be weighed against a fragile peace and an inflation backdrop that has materially shifted.

Equity Markets

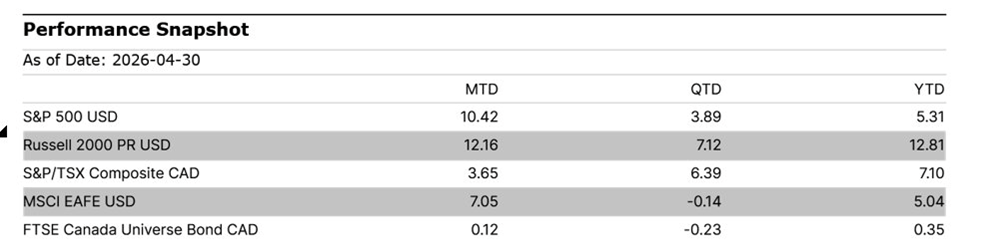

Performance Snapshot as of 2026-04-30.

The S&P 500 USD advanced 10.42% in April to bring its year-to-date return to 5.31%, with the index recovering its prior peak just eleven days after a drawdown that ultimately reached only 9.1%. Sector performance was decidedly skewed toward AI-related names: Communication Services led with an 18.5% gain, followed by Information Technology at 17.5% and Consumer Discretionary at 11.7%. Energy was the notable laggard, retreating 3.5% as oil pulled back from its highs, while Health Care registered a modest 0.4% decline. The Russell 2000 PR USD gained 12.16% in April and is up 12.81% year-to-date, signalling the rally extended well beyond mega-cap technology.

The S&P/TSX Composite CAD advanced 3.65% in April, lifting the index to a 7.10% year-to-date gain. Canadian leadership was concentrated in Health Care, which rose 13.2%, and Financials, which added 10.6%. Industrials, Consumer Discretionary, and Information Technology each gained between 5% and 7%, while Materials declined 5.3% and Communication Services fell 6.5%. Energy posted only a modest 2.0% monthly gain, though year-to-date the sector remains up 32.6% on the strength of higher crude prices. S&P/TSX Small Caps also outperformed, advancing 6.7% in April.

International markets contributed meaningfully to global returns. The MSCI EAFE USD rose 7.05% in U.S. dollar terms (price return) and is up 5.04% year-to-date, while the MSCI Emerging Markets index surged 14.7%, supported by exceptionally strong earnings revisions across tech-intensive Asian markets, where Korean EPS estimates were revised upward by an extraordinary 83% over three months, a magnitude not seen since 1992.

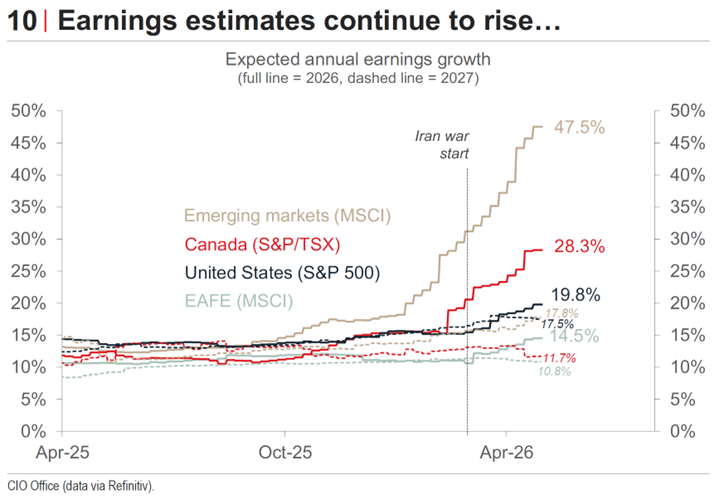

The earnings backdrop remains the principal anchor for the rally. Consensus expectations for 2026 EPS growth now stand at 19.9% for the S&P 500, 14.5% for the S&P/TSX, 28.3% for EAFE, and 47.5% for Emerging Markets. Importantly, 90% of sectors across these regions are posting positive earnings growth, and 75% are growing above their five-year average, a breadth that historically supports continued equity returns.

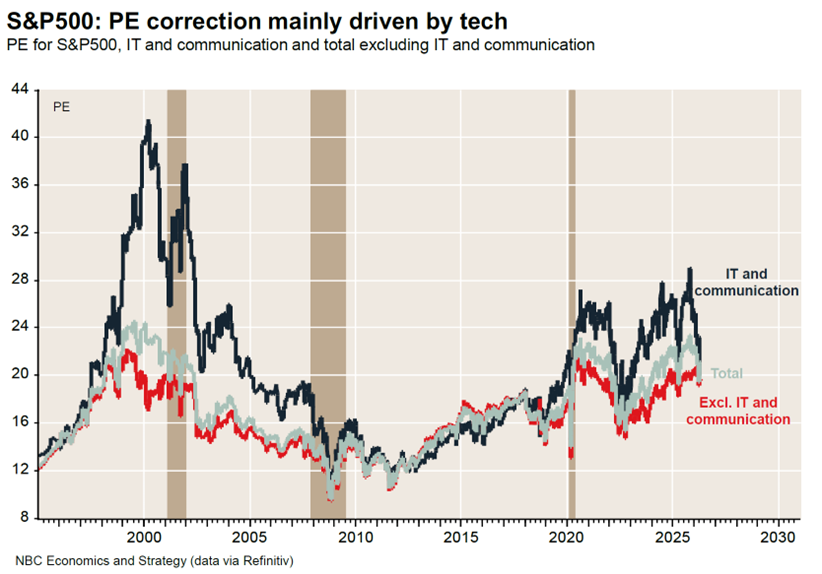

The risks worth acknowledging are valuation-related: while S&P 500 multiples have compressed to a forward P/E of roughly 21x from 23x at year-end, ex-technology valuations near 19.6x remain elevated by historical standards, and analyst earnings revisions of this magnitude have at times preceded periods of disappointment.

Fixed Income and Credit

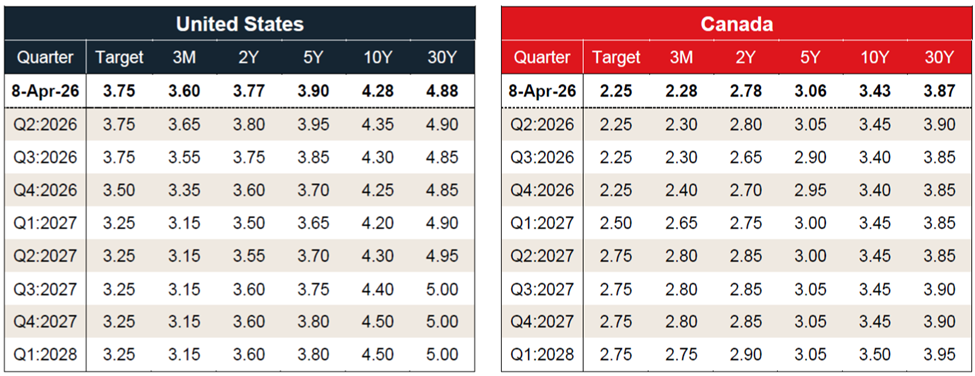

The FTSE Canada Universe Bond CAD was essentially flat in April, returning 0.12% as investors awaited greater clarity on energy prices and inflation, with year-to-date returns of 0.35%. The Bank of Canada held its overnight rate at 2.25% and the Federal Reserve maintained the federal funds target at 3.75%, with both central banks signalling patience. Current expectations point to the Fed resuming rate cuts in December 2026, with a return to neutral at 3.25% slated for 2027, while the Bank of Canada is expected to remain sidelined through 2026 before a modest upward adjustment in early 2027 as economic conditions firm.

The Government of Canada yield curve has bear-flattened since the onset of the Middle East conflict, with 2-year yields up roughly 35 basis points and OIS markets pricing in 38 basis points of BoC tightening by year-end; that pricing appears overly aggressive given the still-fragile labour market and core inflation, which has held below 3% since early 2024. In the United States, the rise in 10-year Treasury yields has been driven primarily by higher real yields rather than breakeven inflation, with the closely watched 5Y/5Y inflation swap actually drifting modestly lower despite the oil shock, a reflection of the market’s enduring confidence in Fed credibility.

Credit markets remained orderly. U.S. investment grade corporates returned 0.6% in April, U.S. high yield gained 1.7%, and Canadian corporate bonds added 0.4% to bring year-to-date returns to 0.7%. Spreads remain tight, and corporate balance sheets are generally healthy, but the combination of elevated valuations and unresolved geopolitical risk reinforces the case for emphasizing higher-quality issuers.

Commodities and Currencies

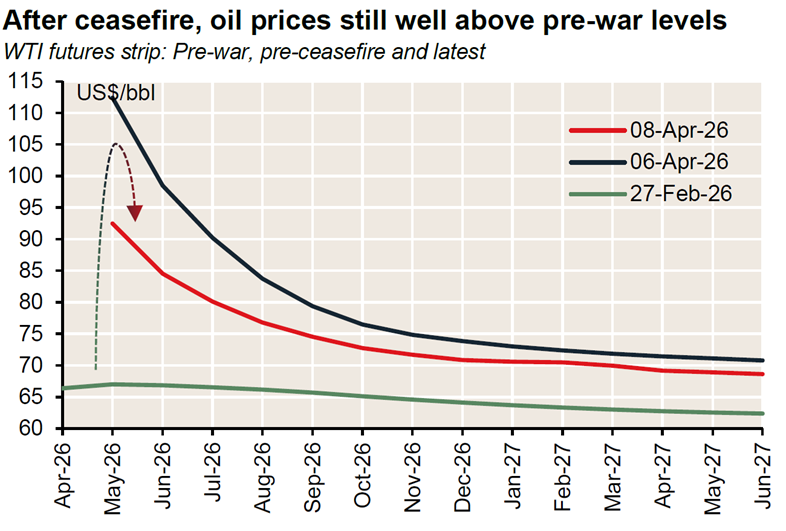

Commodities posted broad-based gains. The GSCI advanced 6.4% on the month and is now up 49.0% year-to-date. WTI crude oil rose 5.6% in April but remains 89.7% higher year-to-date, with the forward curve continuing to embed a meaningful geopolitical premium through at least 2028. Gold was effectively unchanged on the month at -0.1% but holds a 39.6% twelve-month gain, supported by ongoing geopolitical hedging demand and persistent fiscal expansion globally. Copper advanced 5.3% in April and 41.6% over twelve months, with structural demand from AI-related infrastructure build-out providing an additional tailwind alongside cyclical drivers.

Currency markets reflected the easing in geopolitical anxiety. The U.S. dollar index declined 1.9% in April, and the Canadian dollar strengthened 2.4% against the greenback. For Canadian investors holding unhedged foreign assets, the move trimmed reported gains on U.S. and international exposure during a strong month for those markets, a reminder of why thoughtful currency management remains an essential consideration within global portfolios rather than an afterthought.

Economic Overview

United States

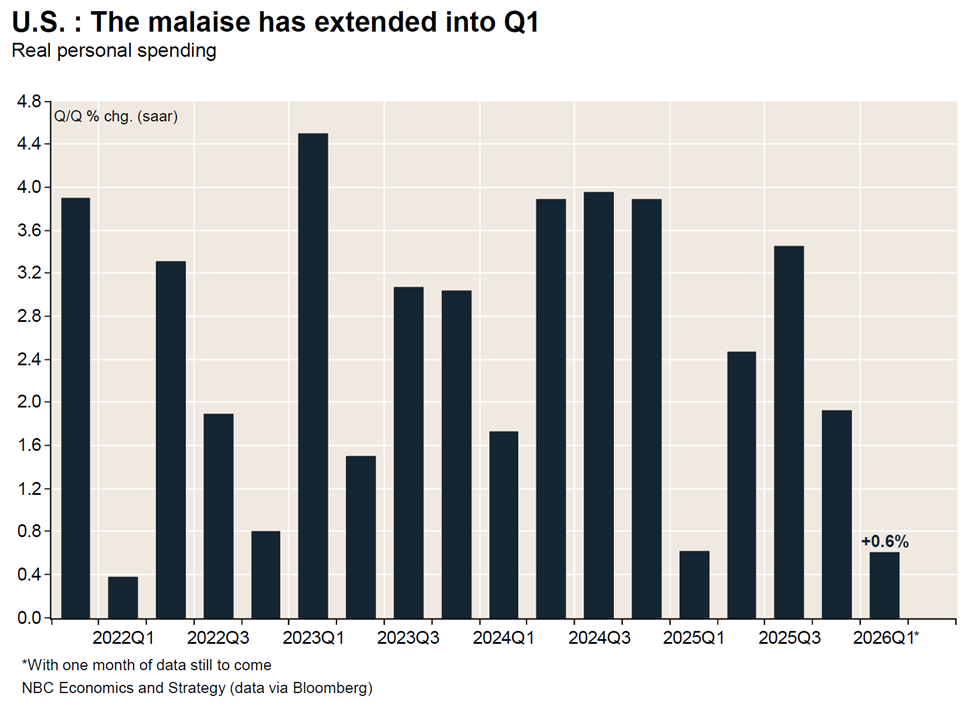

U.S. economic momentum has clearly cooled. The third estimate of fourth-quarter 2025 GDP was revised down sharply to 0.5% annualized from an initial 1.4%, with real personal consumption expenditures tracking only 0.6% in the first quarter, the smallest increase in four years. Real disposable income excluding transfers, one of the four key indicators the NBER uses to date business cycles, has slowed materially. The 2026 U.S. GDP growth forecast has been trimmed to 2.3% from 2.5%, with downside risk if the Middle East situation deteriorates.

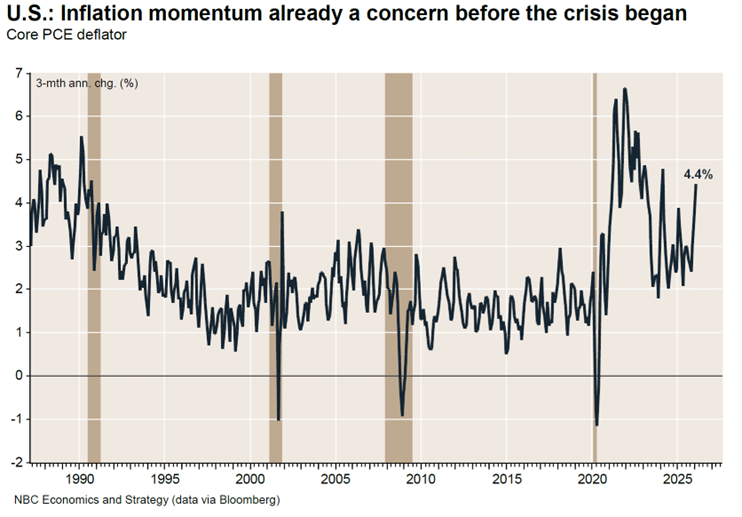

Inflation has moved in the wrong direction. Headline CPI has crossed 3.3%, with the core PCE deflator running at a 4.4% annualized pace over the three months preceding the conflict — the hottest reading outside the post-COVID period since 1990. March energy CPI rose 10.9% month-over-month, the second-fastest gain on record. The University of Michigan consumer sentiment index hit an all-time low in April, reflecting eroding real income expectations.

The labour market is mixed. Headline payroll growth has stalled, but a Dallas Fed analysis suggests the breakeven pace of job creation may now be near zero given the sharp slowdown in unauthorized immigration, meaning the labour market may actually be tightening on the margin. New Federal Reserve Chair Kevin Warsh assumes office in May, and while the case for rate cuts remains in the background, persistent inflation and resilient corporate profit growth argue for continued patience. Fiscal stimulus from the “One Big Beautiful Bill,” together with potential tariff refunds of roughly $166 billion following the February 20 Supreme Court ruling, should provide additional support.

Canada

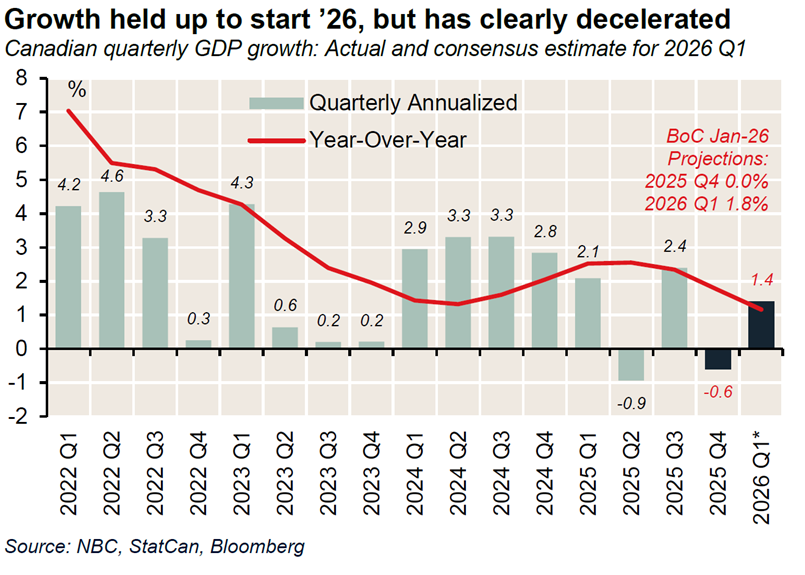

The Canadian outlook is more challenging. Real GDP growth is projected at just 1.0% for 2026, and the labour market is showing strain: employment fell by 95,000 jobs in the first quarter, with manufacturing alone shedding 35,000. Retail and accommodation and food services have also softened. The 2026 CPI forecast has been revised up to 2.5%, though core inflation excluding food and energy has remained below 3% since early 2024 and printed at just 1.9% in March.

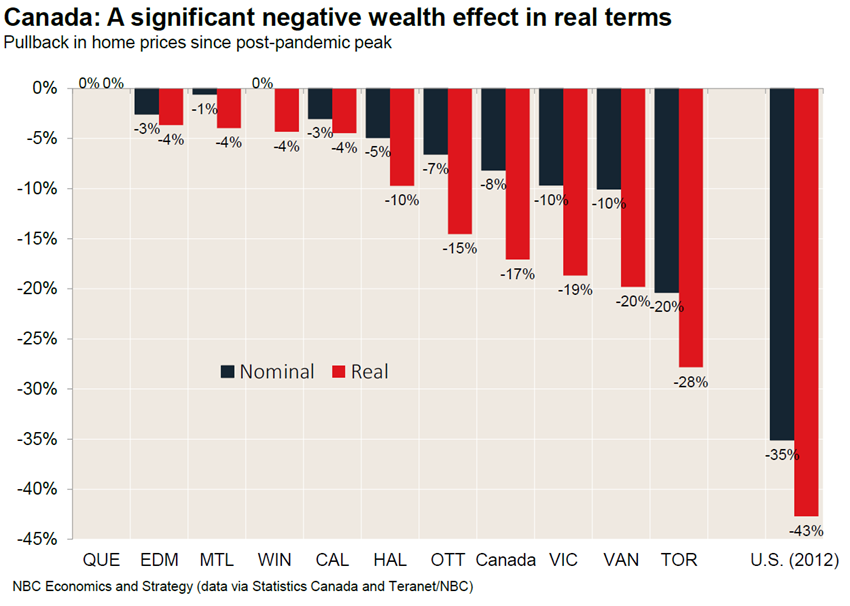

The Bank of Canada is expected to remain on hold through 2026 despite market pricing of roughly 38 basis points of hikes, as Governing Council weighs the temporary inflation impulse against persistent slack. The commodity windfall is bolstering terms of trade, public finances, and resource-sector profits; federal nominal GDP could come in near 5% versus a 3% budget assumption, but the resource sector is not labour-intensive enough to offset weakness elsewhere. Real home prices are down 6.5% year-over-year, with Toronto and Vancouver off 28% and 20% respectively in real terms from their post-pandemic peaks. Population decline, sluggish housing activity, and the upcoming CUSMA review continue to weigh on the outlook.

Bottom Line

April reinforced a pattern that has defined the past six years: equity markets have repeatedly demonstrated an ability to look through extraordinary disruption, including a pandemic, an inflation shock, tariff turmoil, and now an energy supply shock, without waiting for a full return to normalcy. Broad-based earnings growth, a labour market in rough balance, and credible central banks have provided the foundation, while AI-related investment continues to drive earnings dispersion in favour of technology-heavy markets.

The risks ahead deserve equal weight. Oil prices remain near $100 per barrel and the Strait of Hormuz is still effectively closed, leaving the inflation path and central bank reaction functions less certain than markets appear to assume. U.S. equity valuations outside of technology are stretched, Canadian housing weakness continues to weigh on household balance sheets, and the CUSMA review introduces another layer of trade-policy risk for Canadian investors. Earnings growth in the 15% to 20% range, while constructive on its face, has historically been associated with more modest forward returns as the bar for upside surprise rises.

Against this backdrop, we remain focused on maintaining diversification across regions, sectors, and asset classes; emphasizing quality investments capable of compounding through volatility; and preserving flexibility within portfolios so that we can adapt as the outlook becomes clearer. A measured approach to risk-taking remains appropriate: disciplined enough to participate in a constructive earnings environment and flexible enough to navigate the headwinds that persist.

Sources Used

• CIO Office, Asset Allocation Strategy: The Resilience Paradox, May 1, 2026.

• Economics and Strategy, Monthly Fixed Income Monitor, April 2026.

• Economics and Strategy, Monthly Equity Monitor, May 2026.

• Economics and Strategy, Monthly Economic Monitor: U.S. Less growth… and more inflation, April 2026.

• Economics and Strategy, Monthly Economic Monitor: Canada. Can the commodities boom revitalize the economy? April 22, 2026.