InsightsMonthly Market Wrap – June 2026

July 08, 2026 • 10 MIN READ

Key Takeaways

EQUITIES CLOSED A STRONG FIRST HALF

Despite a choppier June, the S&P/TSX Composite gained 6.37% for the quarter and 9.92% year to date, while emerging markets led global returns as the U.S.–Iran agreement eased the year’s dominant risk.

BONDS ADVANCED AS INFLATION EXPECTATIONS EASED

The FTSE Canada Universe Bond Index returned 0.51% in June, with the Bank of Canada firmly on hold and the Federal Reserve facing renewed tightening speculation.

NORTH AMERICAN ECONOMIES ARE DIVERGING

Resilient U.S. growth powered by artificial intelligence investment contrasts with a Canadian economy exiting a shallow technical recession and tracking a firmer second quarter.

EARNINGS EXPECTATIONS HAVE BECOME AMBITIOUS

Double-digit profit growth is now priced into every major region and U.S. index concentration sits at record levels, keeping quality and selectivity at a premium.

THE U.S. DOLLAR STRENGTHENED; THE CANADIAN DOLLAR SLIPPED

The U.S. dollar strengthened and the Canadian dollar weakened roughly 1.6%, a tailwind for the Canadian-dollar value of unhedged foreign holdings.

POSITIONING REMAINS NEUTRAL BUT OPPORTUNISTIC

Bottom line: we remain constructive on equities while staying diversified, quality-focused, and flexible, given elevated concentration, geopolitical, and policy risks.

Introduction

June brought a measure of resolution to the question that dominated the first half of 2026. The agreement between the United States and Iran, and with it the gradual reopening of the Strait of Hormuz, sent oil prices sharply lower and allowed markets to refocus on fundamentals. Equities capped a strong quarter, bonds benefited from easing inflation expectations, and the U.S. dollar extended its rally to a yearly high. The second half brings its own complexity to navigate, including sticky U.S. inflation, a Federal Reserve flirting with tightening, and elevated expectations for AI-driven earnings, but investors enter it with the year’s most acute risk having receded.

Equity Markets

Performance as of June 30th, 2026

| Index | 1-Month | 3-Month | Year-to-Date |

| S&P/TSX Composite | 0.25% | 6.37% | 9.92% |

| S&P 500 (USD) | -1.06% | 14.87% | 9.55% |

| Russell 1000 Growth (USD) | -2.74% | 16.57% | 5.02% |

| Russell 2000 (USD) | 3.60% | 21.15% | 21.86% |

| MSCI EAFE (USD) | -0.03% | 9.80% | 7.74% |

| FTSE Canada Universe Bond | 0.51% | 2.01% | 2.24% |

| Gold (USD) | −11.47% | −12.72% | -6.73% |

| USD/CAD | 2.64% | 2.37% | 3.49% |

Index total returns for periods ended June 30, 2026. Source: performance table provided.

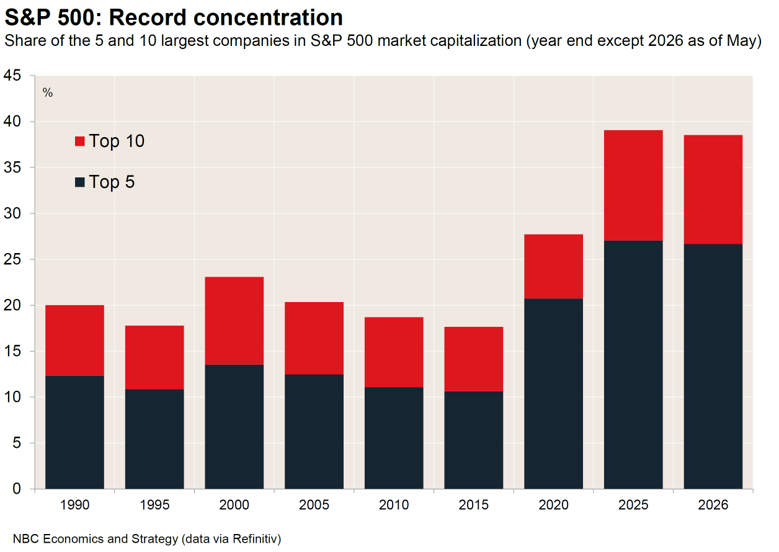

The S&P 500 slipped 1.06% in June yet still delivered a 14.87% gain for the second quarter, bringing its year-to-date advance to 9.55%. Notably, the month’s weakness was concentrated where gains had been hottest, with information technology retreating 3.3% after a 31.8% quarterly surge, while industrials (+7.3%), health care (+6.6%) and financials (+4.4%) led, a rotation that speaks to healthy breadth rather than deteriorating fundamentals. That broadening is also visible across the size spectrum: the Russell 2000 added 3.60% in June and has now returned 21.86% year to date, comfortably ahead of the large-cap benchmark, while the Russell 1000 Growth index fell 2.74% on the month. Concentration nevertheless remains a defining feature of this market, with the ten largest S&P 500 constituents representing roughly 40% of index capitalization.

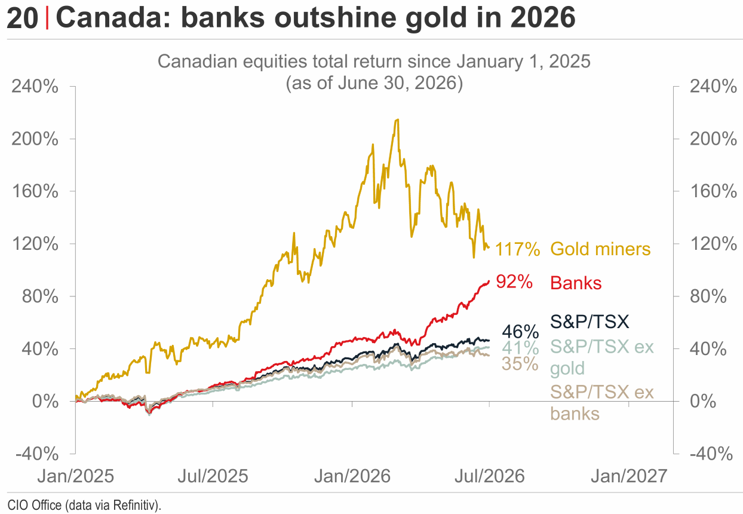

Canadian equities continued to climb a wall of domestic worry. The S&P/TSX Composite added 0.25% in June, capping a 6.37% quarter and a 9.92% year-to-date gain despite an economy that has barely grown. Financials did the heavy lifting, rising 8.8% in the month and 25.6% over the quarter, with the banks now up more than 30% this year on stronger capital markets activity, improving returns on equity and a more growth-friendly policy backdrop in Ottawa. Energy eased 4.1% in June alongside falling crude prices but remains up 23.6% for the year, while materials fell 12.1% as the pullback in bullion weighed heavily on gold producers. We would note that bank valuations have reached their richest levels since 2008 in remarkably short order, which argues for tempering expectations from here.

International markets rounded out a constructive quarter. The MSCI EAFE index was essentially flat in June at -0.03% but has returned 7.74% year to date in U.S. dollar terms, while emerging markets remain the global leaders, up roughly 24% this year on the strength of AI-exposed Emerging Asia, which surged 28% in the second quarter alone. The path has not been smooth, as an 8% single-session plunge in Korean equities in early June, quickly recovered, illustrated how sensitive the AI trade has become to shifting sentiment.

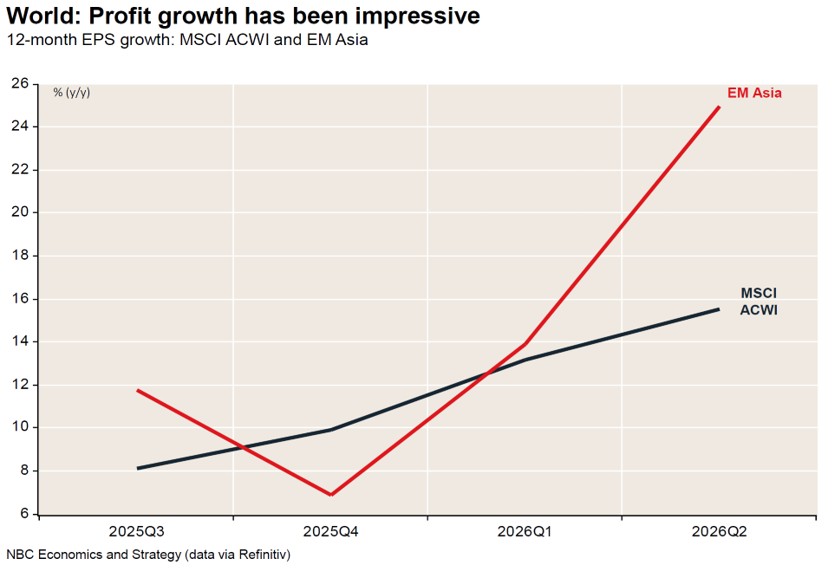

Earnings will need to carry the load from here. Consensus now embeds double-digit profit growth across every major region over the next twelve months, including roughly 20% for global equities and a striking 40% for Emerging Asia. With equity risk premiums unusually compressed, delivery against those expectations, rather than further multiple expansion, is likely to determine second-half returns, reinforcing the case for selectivity and quality.

Fixed Income and Credit

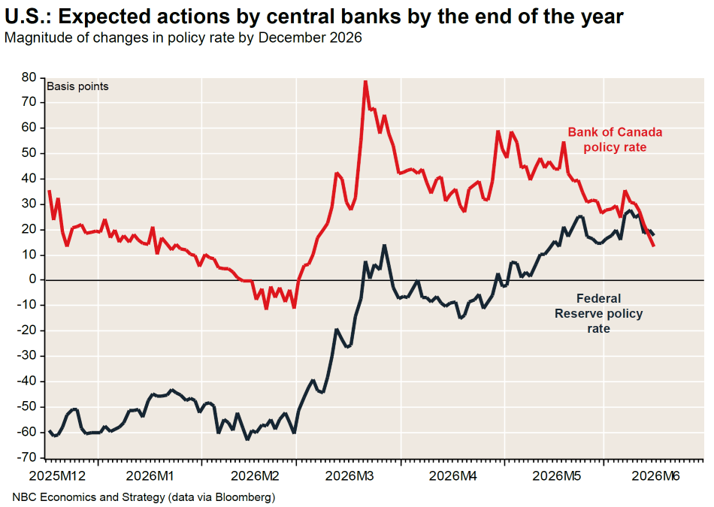

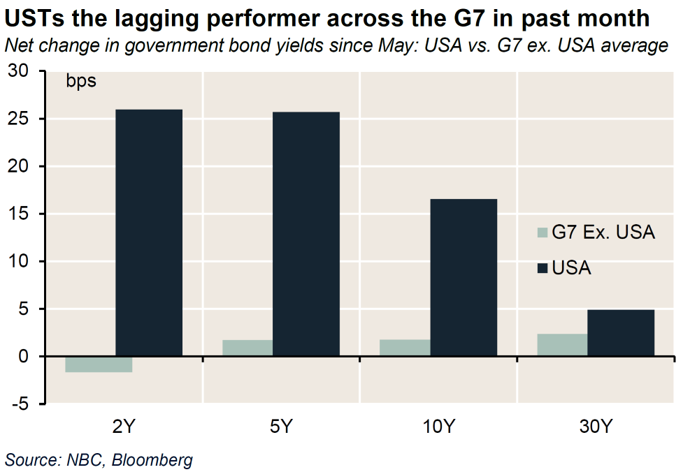

Canadian bonds delivered a solid month, with the FTSE Canada Universe Bond Index returning 0.51% in June to bring its quarterly and year-to-date gains to 2.01% and 2.24%, respectively, as normalizing energy prices pushed inflation expectations and yields lower. The Bank of Canada held its overnight rate at 2.25% and, in our view, is well positioned to remain sidelined through year-end, looking through the energy-driven bump in headline inflation. The contrast with the United States is stark: the federal funds target sits at 3.75%, and markets have moved from pricing multiple cuts at the start of the year to discounting the possibility of hikes by December, with modest odds of a first move as early as July.

That divergence is anchored in inflation. Core prices excluding food and energy are rising just 1.5% year over year in Canada, against a core PCE reading of 3.4% in the United States, giving the Bank of Canada room the Federal Reserve simply does not have. Meanwhile, elevated term premiums, reflecting fiscal deterioration, questions around central bank leadership and lingering geopolitical uncertainty, are likely to keep long U.S. Treasury yields high, with the 30-year expected to hold above 5% over the coming year. Canadian long bonds look comparatively well supported, with better-contained inflation and a stronger fiscal position pointing to continued outperformance versus Treasuries at the long end.

Credit remained firm. Canadian corporate bonds returned 0.3% in June and 2.2% year to date, while U.S. high yield gained 2.5% over the quarter. Balance sheets are broadly healthy, but with spreads offering limited compensation for risk, we continue to emphasize quality issuers and selectivity rather than reaching for yield.

Commodities and Currencies

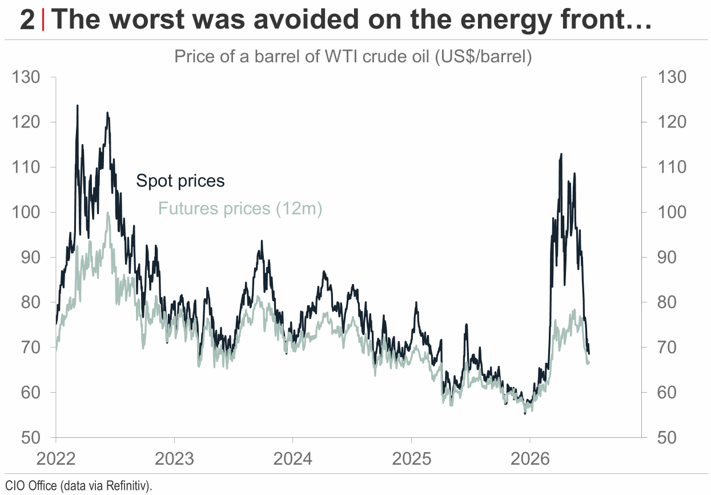

Energy dominated the commodity story. WTI crude fell 22.6% in June, and 31.4% over the quarter, as markets priced the gradual reopening of the Strait of Hormuz, though prices remain up 23.2% year to date and above pre-conflict levels given low global inventories and a reopening that will take months to complete. Gold declined 11.47% in June and is now down 6.73% for the year, more than 20% below its March peak, as a stronger U.S. dollar and hawkish rate repricing drained momentum from bullion; we continue to see a US$4,000–US$6,000 range as reasonable over the next 12 to 36 months. Copper, up 7.2% year to date, remains supported by electrification and data-centre demand tied to the AI buildout.

Currency moves were consequential for Canadian investors. The broad U.S. dollar index rose 2.3% in June and USD/CAD climbed 2.64%, pushing above 1.42 for the first time since spring 2025 as rate differentials widened and two of Canada’s trade pillars, gold and oil, softened. The weaker loonie flattered unhedged foreign returns this year and cushioned June’s pullback in U.S. equities. We expect the tide to turn gradually, with USD/CAD forecast at 1.37 by year-end and 1.33 by the first quarter of 2027 as trade clarity improves, an outlook that argues for disciplined currency management rather than chasing recent dollar strength.

Economic Overview

United States

The U.S. economy continues to expand at an above-potential pace, with real GDP up 2.6% year over year and growth expected to reach 2.3% in 2026 and 2.1% in 2027. Artificial intelligence remains the engine: sectors most exposed to the technology have grown a cumulative 56.6% since late 2022, against 17.0% for the rest of the economy, and hyperscaler capital spending plans continue to climb. Consumer spending has held up despite a savings rate that fell to a 46-month low of 2.6% in April, with tariff reimbursements, already totalling roughly US$30 billion following the Supreme Court ruling, providing an additional offset.

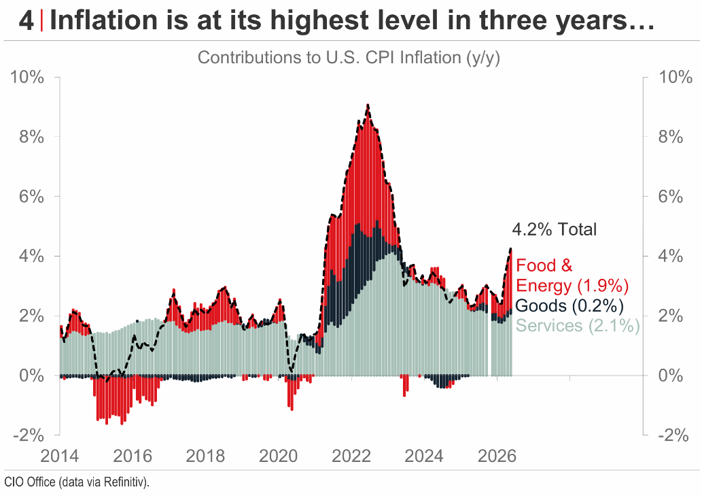

Inflation is the complication. Headline CPI reached a three-year high of 4.2% in May, with core at 2.9%, while the PCE deflator, the Federal Reserve’s preferred gauge, ran at 4.1% headline and 3.4% core. Falling energy prices should pull headline readings lower through the second half, but AI-related categories, including electricity (+5.9%) and computer software and accessories (+12.8%), illustrate pressures that will not fade with the Strait of Hormuz reopening.

The labour market, meanwhile, has cooled without cracking. June payrolls rose just 57,000, well below expectations, with prior months revised down by a cumulative 74,000 and the household survey showing an outright decline in employment. Still, payroll growth has averaged 111,000 over the past three months, sufficient against a much slower flow of new labour-market entrants. A labour market neither hot enough to compel tightening nor weak enough to justify easing supports our view that the federal funds rate stays on hold over the next twelve months, even as half of Fed officials project higher rates this year.

Canada

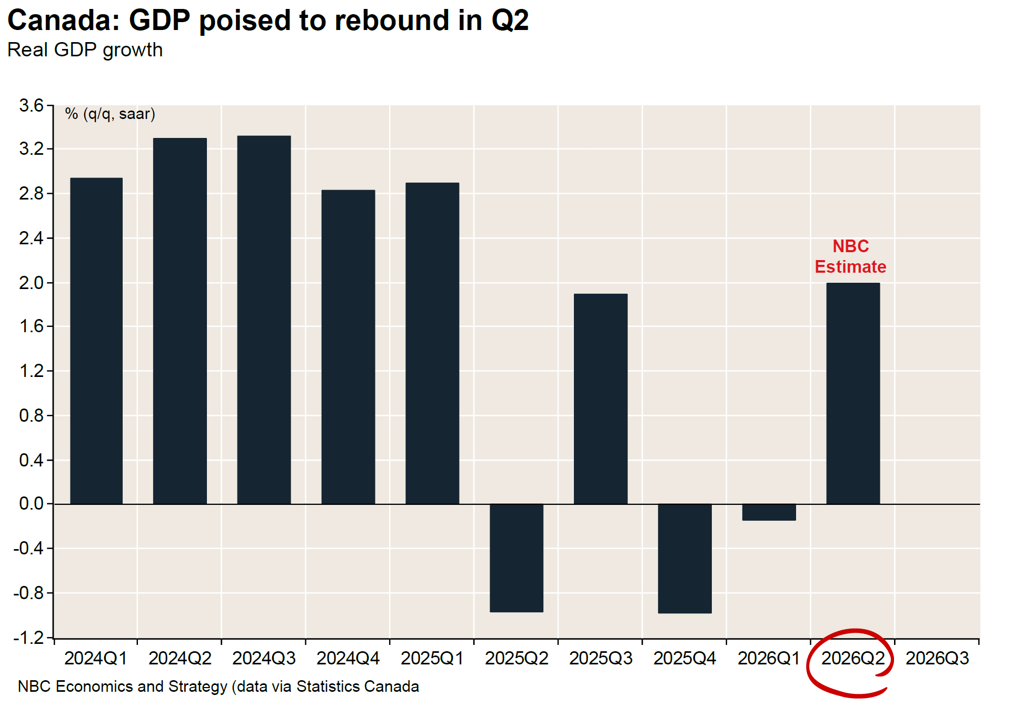

Canada’s first quarter contraction of 0.1% annualized, following a 1.0% decline in late 2025, met the definition of a technical recession, but the label overstates the damage. The downturn was neither pronounced, persistent nor pervasive by historical standards, and the economy has since turned: real GDP rose 0.5% in April, with output expanding in 14 of 20 industries, and the second quarter is tracking annualized growth of roughly 2.3%. Even so, the soft start prompted a downward revision to 2026 growth expectations, now 0.7% for the year.

The labour market echoes that mixed picture. May delivered the fastest job growth in 17 months, though the trend this year remains essentially flat and the unemployment rate has been rangebound between 6.5% and 7.0%. Wage growth has slowed to 2.6%, a multi-year low, and core inflation excluding food and energy sits at just 1.5%, evidence of lingering slack that keeps the Bank of Canada comfortably on the sidelines.

Trade policy remains the swing factor. Washington’s July 1 move toward repeated annual reviews of CUSMA leaves Canadian exporters under a persistent cloud, although sticky U.S. inflation and looming midterm elections give the administration a clear incentive to restore certainty, and we continue to expect a resolution by year-end. Encouragingly, Ottawa has deployed its most pro-growth agenda in more than a decade, spanning the National Electricity Strategy, a 932-megawatt data-centre project near Edmonton and the newly approved one-million-barrel-per-day pipeline to the British Columbia coast, initiatives that brighten the medium-term investment outlook even as the population declined for a third consecutive quarter.

Bottom Line

June confirmed that the worst-case scenario for 2026 has been avoided. De-escalation in the Middle East, falling energy prices and resilient growth allowed nearly every asset class to close the first half in positive territory, and the macroeconomic backdrop continues to favour equities over fixed income.

The risks ahead are real but navigable. Earnings expectations are ambitious, index concentration is extreme and equity risk premiums are compressed, leaving little margin for disappointment in the AI investment cycle. Sticky U.S. inflation could yet push the Federal Reserve into tightening, and the shift to annual CUSMA reviews prolongs uncertainty for Canadian trade and investment.

Against that backdrop, we continue to remain neutral on equities and would view any upcoming weakness as a potential buying opportunity, particularly in areas where enthusiasm has run furthest ahead of fundamentals. Our approach remains unchanged: maintaining diversification, emphasizing quality investments, and preserving flexibility within portfolios so that we can respond as the second half unfolds.

Sources Used

• Performance Table – June 30, 2026 (authoritative index returns)

• Monthly Equity Monitor – June 2026 (Economics and Strategy)

• Monthly Fixed Income Monitor – June 2026 (Economics and Strategy)

• Monthly Economic Monitor U.S. – June 2026 (Economics and Strategy)

• Monthly Economic Monitor Canada – June 2026 (Economics and Strategy)

• Forex – July 2026 (Economics and Strategy)

• CIO Office Asset Allocation Strategy – July 2026