InsightsMonthly Market Wrap – May 2026

June 09, 2026 • 10 MIN READ

Key Takeaways

EQUITIES RALLIED BROADLY IN MAY

Equities led again. The S&P 500 rose 5.15% and the S&P/TSX 2.37% on the month, while emerging markets jumped 9.7%, with AI-related technology names doing most of the heavy lifting.

BONDS EDGED HIGHER, BUT U.S. TREASURIES LAGGED

Bonds posted modest gains, with the FTSE Canada Universe Bond up 1.36%, though U.S. Treasuries lagged as markets shifted toward pricing a possible Fed rate hike rather than cuts.

INFLATION AND RATE POLICY ARE DIVERGING ACROSS BORDERS

U.S. inflation is reaccelerating and the Federal Reserve is on hold; Canadian growth is soft but inflation remains contained, with the Bank of Canada also on hold.

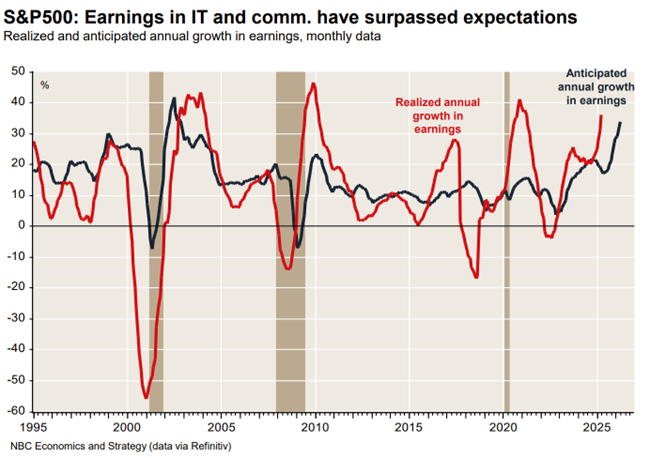

EARNINGS GROWTH, NOT VALUATION EXPANSION, IS DRIVING THE GAINS

The gains were driven by genuine earnings growth rather than richer valuations, but they have become increasingly concentrated in a handful of AI winners.

THE U.S. DOLLAR STRENGTHENED; THE CANADIAN DOLLAR SLIPPED

The U.S. dollar strengthened and the Canadian dollar weakened roughly 1.6%, a tailwind for the Canadian-dollar value of unhedged foreign holdings.

POSITIONING REMAINS CONSTRUCTIVE BUT DISCIPLINED

Bottom line: we remain constructive on equities while staying diversified, quality-focused, and flexible, given elevated concentration, geopolitical, and policy risks.

Introduction

Global markets extended their advance in May, with equities pushing higher even as the Strait of Hormuz disruption kept oil elevated and geopolitical risk firmly in view. The dominant theme remained the resilience of corporate earnings, particularly across artificial-intelligence leaders, which carried U.S. and emerging-market indices to fresh highs. Investor sentiment stayed constructive on prospects for a durable U.S.–Iran de-escalation and on continued upward earnings revisions, though the tone in fixed income and currency markets was more guarded as a repricing of central bank expectations lifted the U.S. dollar. The month underscored a market climbing a wall of worry, leaving investors to navigate concentration, persistent inflation, and an unusually uncertain monetary policy backdrop in the months ahead.

Equity Markets

Performance as of May 31st, 2026

Total returns by index; USD/CAD shown as currency change. Periods ended May 31, 2026.

| Index | 1-Month | 3-Month | Year-to-Date |

| S&P/TSX Composite | 2.37% | 1.25% | 9.64% |

| S&P 500 (USD) | 5.15% | 10.19% | 10.73% |

| Russell 1000 Growth (USD) | 7.19% | 13.70% | 8.14% |

| Russell 2000 (USD) | 4.27% | 10.90% | 17.62% |

| MSCI EAFE (USD) | 2.60% | −1.96% | 7.77% |

| FTSE Canada Universe Bond | 1.36% | −0.51% | 1.72% |

| Gold (USD) | −1.54% | −13.77% | 5.25% |

| USD/CAD | 1.59% | 0.94% | 0.58% |

U.S. equities led global markets in May, with the S&P 500 USD advancing 5.15% on the month to bring its year-to-date gain to 10.73% and its trailing three-month return to 10.19%. Leadership remained concentrated at the sector level, where information technology surged 16.0% as AI-related earnings revisions continued to broaden, while more cyclical areas lagged, with energy down 5.6%, utilities off 5.1%, and consumer staples lower by 3.2%. Style and size told a more nuanced story: the Russell 1000 Growth USD rose 7.19% as growth leadership persisted, yet firmer small-caps, with the Russell 2000 USD gaining 4.27% on the month and leading year-to-date at 17.62%, pointed to some broadening beneath the surface.

Canadian equities posted more measured gains, with the S&P/TSX Composite rising 2.37% in May to extend its year-to-date return to 9.64%, the softer three-month figure of 1.25% reflecting a choppier spring. Resource and rate-sensitive sectors did the heavy lifting: communication services advanced 6.9%, materials gained 6.2% on firmer metals, and financials rose 4.4%. Energy lagged at -2.8% alongside softer crude, and health care fell 5.0%.

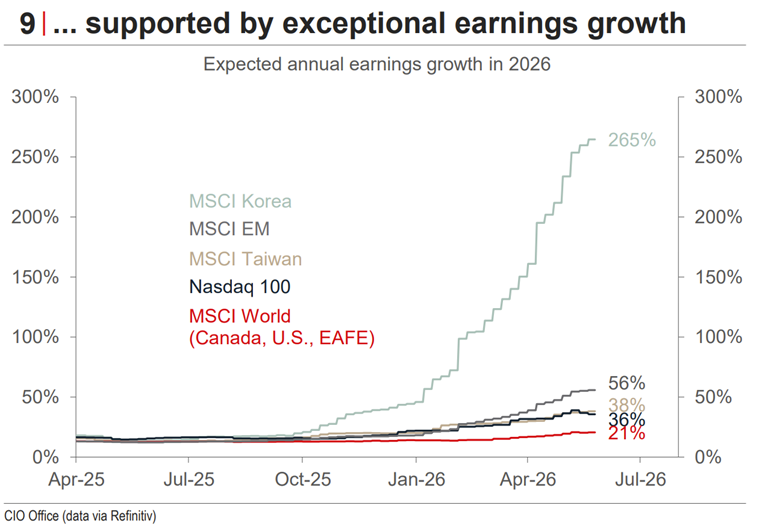

Internationally, developed markets outside North America trailed, with the MSCI EAFE USD advancing 2.60% in May and 7.77% year-to-date while remaining marginally negative over three months. The clear standout was emerging markets, where the MSCI Emerging Markets USD jumped 9.7% on the month and 25.7% year-to-date. The emerging-market rally has been driven overwhelmingly by Asian technology leaders tied to the AI supply chain, a transformation that has lifted both earnings and index weight but has also raised the degree of concentration around a single theme.

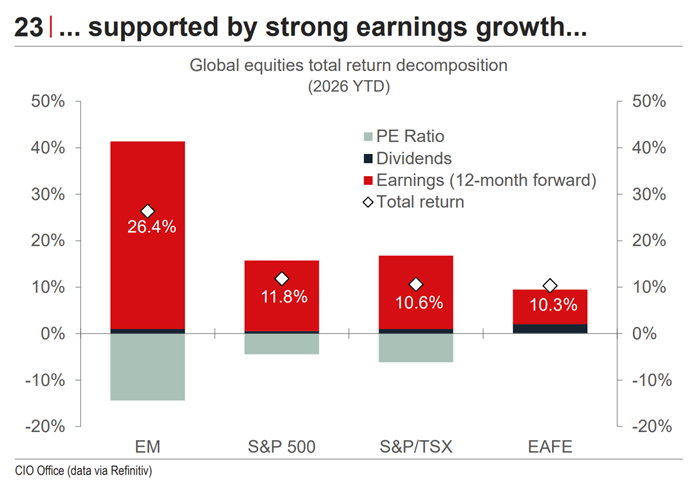

The broader equity advance has rested on fundamentals rather than multiple expansion. On a year-to-date basis, returns across most regions have come from higher forward earnings, with forward price-to-earnings ratios actually contracting; the scale of positive earnings revisions for global equities ranks among the strongest in a generation. The risks lie in sustainability: consensus estimates may be anchoring to recent upside surprises, AI-related capital spending faces grid and financing constraints, and a prolonged commodity-price premium could pressure margins and real incomes.

Fixed Income and Credit

The Canadian fixed income universe ended a volatile month on firmer footing, with the FTSE Canada Universe Bond index returning 1.36% in May to bring its year-to-date gain to 1.72%, supported by lower energy prices and a run of softer-than-expected Canadian data, though the index remained marginally negative over the trailing three months at -0.51% following the spring backup in yields. Both central banks held steady, leaving the Bank of Canada’s policy rate at 2.25% and the Federal Reserve’s at 3.75%, with the Bank widely expected to remain on the sidelines through year-end and the Fed signalling no near-term move in either direction.

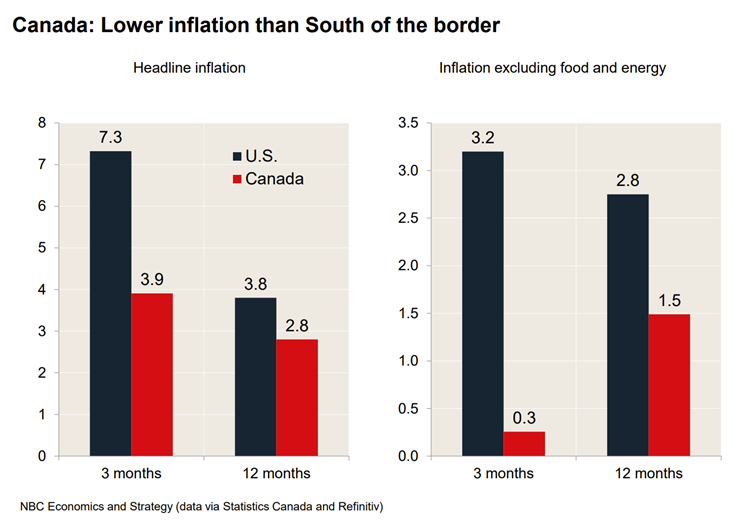

The more notable development was a growing divergence in the inflation backdrop across borders, which increasingly underpins differences in rate expectations. As illustrated, inflation in the United States remains meaningfully higher than in Canada, with headline CPI running at 7.3% on a three-month annualized basis versus 3.9% in Canada. The gap is even more pronounced on a core basis, where U.S. inflation sits at 3.2% compared to just 0.3% in Canada over the same period.

This divergence helps explain the contrasting bond market behaviour. Persistent inflationary pressure in the U.S. continues to challenge the Federal Reserve’s ability to ease policy, contributing to higher Treasury yields and elevated term premia. By contrast, more contained inflation in Canada supports a steadier policy outlook for the Bank of Canada and has helped anchor domestic yields, reinforcing the relative outperformance of Canadian fixed income markets.

Commodities and Currencies

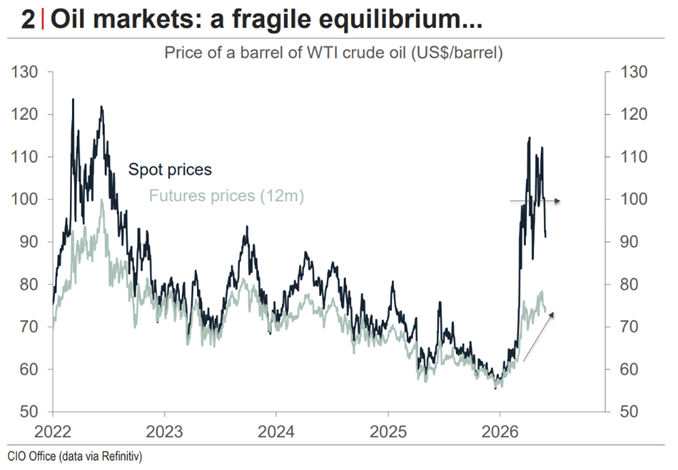

Commodities were the weakest corner of markets in May, with the broad GSCI USD index down 7.6%. The decline was led by crude, where WTI fell 16.1% on the month even as it held a 59.2% year-to-date gain, a reminder that the Strait of Hormuz premium remains embedded in prices despite the monthly pullback. Gold eased 1.54% in May but retains a 5.25% year-to-date advance, though it has given back 13.77% over the past three months, while copper rose 4.6%, supported in part by the structural demand tailwind from AI-driven electrification and data-centre buildout. For Canadian portfolios, firm base metals and still-elevated bullion continue to underpin the resource-heavy domestic index.

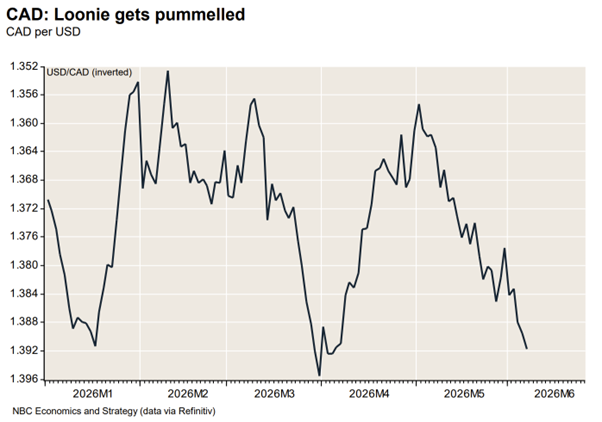

In currencies, the U.S. dollar regained ground, with the DXY index up 0.9% in May as the hawkish repricing of Fed expectations outweighed the usual risk-on headwind from rising equities. The Canadian dollar was among the weakest major currencies, depreciating roughly 1.6% against the U.S. dollar on the month, with USD/CAD moving back toward 1.39 on a deteriorating real growth profile, an unfavourable Canada–U.S. rate spread, and softer bullion. A weaker loonie flatters the CAD value of unhedged foreign holdings, a meaningful tailwind for Canadian investors given the strength of U.S. and emerging-market returns, and reinforces the case for deliberate currency management within globally diversified portfolios.

Economic Overview

United States

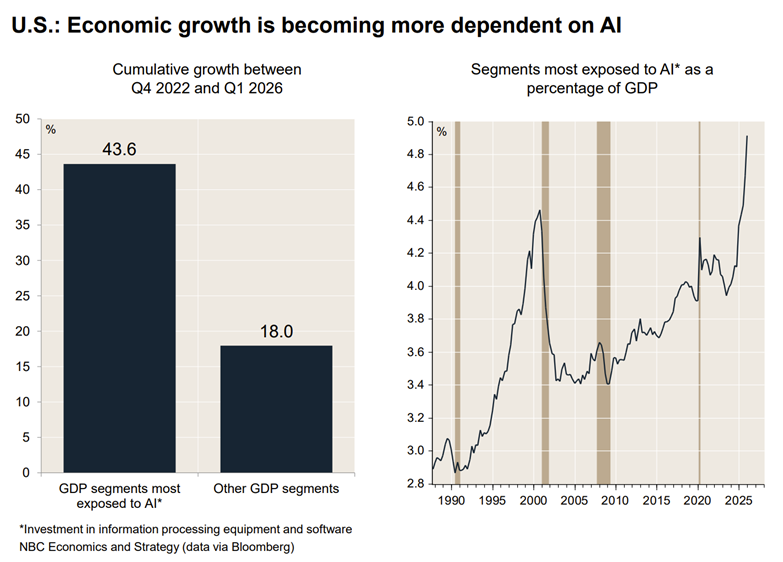

The U.S. economy expanded at a 2.0% annualized pace in the first quarter, with the headline figure understating underlying momentum; final sales to private domestic purchasers rose a solid 2.5% as the drag came largely from a surge in imports tied to AI-related equipment. Business investment remained the standout, with information-processing equipment up 43.4% annualized, underscoring how dependent growth has become on the AI capital-spending cycle. Forward growth is expected to hold above potential, with real GDP projected at 2.4% in 2026 and 2.0% in 2027.

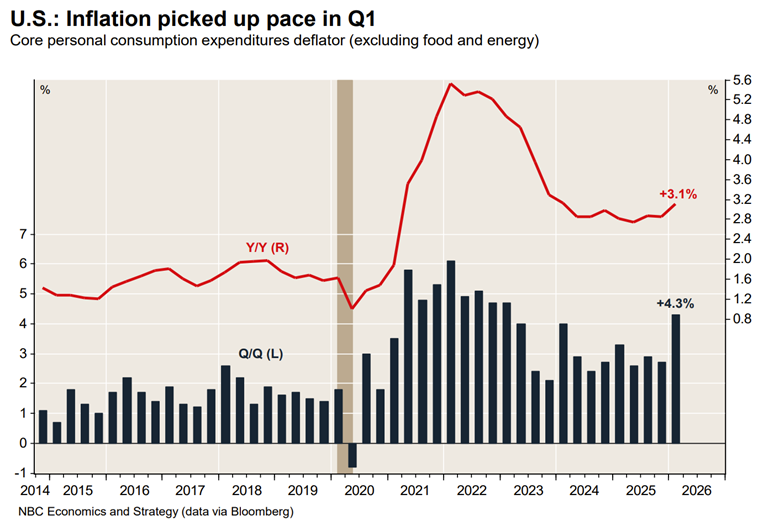

Inflation, however, is reaccelerating. The core PCE deflator rose at a 4.3% annualized rate in the first quarter, lifting the twelve-month figure to a two-year high of 3.1%, with elevated energy prices and electronics costs feeding through. The labour market has firmed, with private hiring regaining momentum and initial jobless claims at their lowest since early 2024, even as consumer confidence fell to a record low in May. Against this backdrop, the Federal Reserve under new Chair Kevin Warsh held rates at 3.75% and markets no longer price cuts this year, with the risk skewed toward overheating rather than easing.

Canada

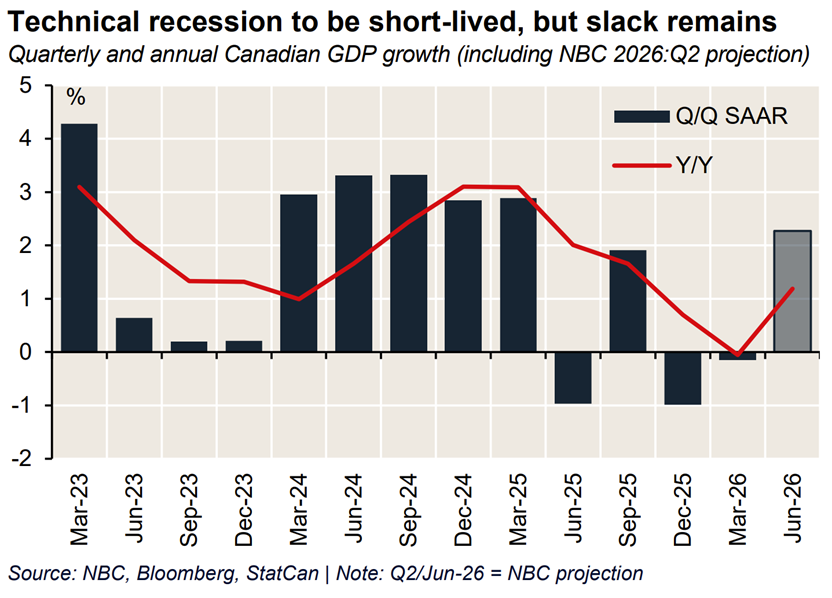

Canada’s growth profile has softened, with the economy recording two consecutive quarters of contraction and headlines flagging a technical recession, though the first-quarter decline was modest and second-quarter activity is tracking above 2%. Full-year GDP is projected to grow 1.0% in 2026, supported by an assumed renewal of CUSMA, which remains both the most likely scenario and the principal risk to the outlook. The Bank of Canada is expected to hold its policy rate at 2.25% through year-end.

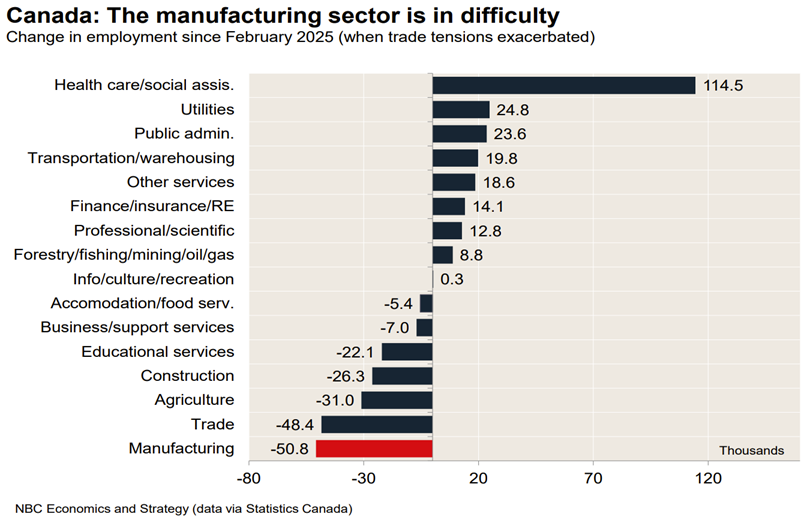

Inflation tells a more benign story than south of the border. Headline CPI is expected to peak near 3% on rising gasoline prices before gradually disinflating, while the Bank’s preferred core measures eased to a 63-month low around 2.05%, contrasting sharply with U.S. core inflation. The labour market remains soft despite a 154,000 jump in full-time positions in May; year-to-date job creation is effectively flat and the unemployment rate has held between 6.5% and 7.0%. Manufacturing has borne the brunt of trade tensions, with widespread losses concentrated in U.S.-dependent and Quebec-based industries, and population decline is adding a further drag on domestically oriented demand.

Bottom Line

The defining feature of May was the resilience of equity markets, which advanced despite an unresolved energy shock and persistent geopolitical risk. What is working is earnings: the rally has been driven by genuine profit growth and broad-based upward revisions rather than multiple expansion, with AI leaders and emerging-market technology names at the centre of the move and most major indices trading at valuations below where they began the year.

The risks are equally clear and warrant acknowledgement. Equity gains have grown increasingly concentrated around a single AI theme, valuations in parts of the technology complex remain demanding, and the Strait of Hormuz stalemate could yet disrupt supply more broadly. Compounding this is an unusually uncertain monetary backdrop, with inflation reaccelerating in the United States, markets pricing potential rate hikes, and a new Federal Reserve Chair still untested by markets, alongside the unresolved CUSMA review that hangs over the Canadian outlook.

In this environment, we remain constructive but disciplined. The appropriate response is not to chase momentum but to position deliberately: maintaining diversification across regions and asset classes, emphasizing quality investments with durable earnings and sound balance sheets, and preserving flexibility within portfolios so that we can respond as the geopolitical and policy picture evolves.

Sources Used

• Verus Financial Performance Table — periods ended May 31, 2026 (index total returns and USD/CAD).

• Asset Allocation Strategy, CIO Office, National Bank Investments — June 2026 (sector performance, EM returns, asset allocation views, bond-market analysis).

• Monthly Equity Monitor, Economics and Strategy — May 2026 (global earnings revisions, valuation analysis, sector rotation, market forecasts).

• Monthly Fixed Income Monitor, Economics and Strategy — June 2026 (Fed and BoC policy outlook, yield forecasts, Treasury underperformance).

• Monthly Economic Monitor – U.S., Economics and Strategy — May 2026 (Q1 GDP, AI investment, core PCE, labour market, forecasts).

• Monthly Economic Monitor – Canada, Economics and Strategy — May/June 2026 (growth, labour market, inflation, trade and CUSMA risk).

• Forex, Economics and Strategy — June 2026 (USD, CAD, EUR and CNY analysis; policy rates; currency forecasts).